作者:黄可心

来源:杨仁文研究笔记

事件:

公司8月13日发布19H1财报,收入14.85亿元,同比上升16.1%。归母净利润1.10亿元,同比下降35.4%,EPS 3.4分。

点评:

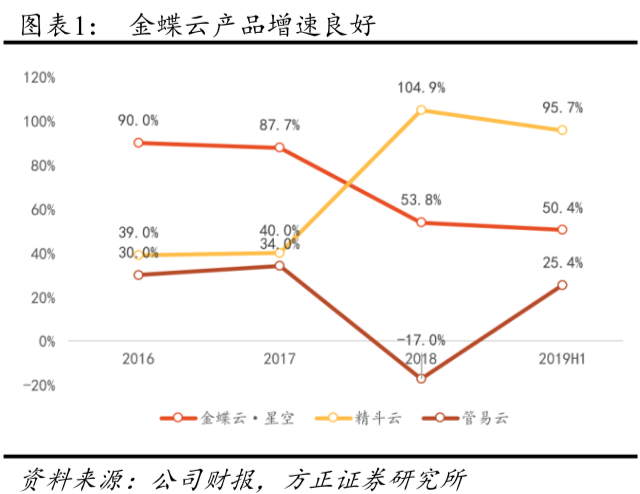

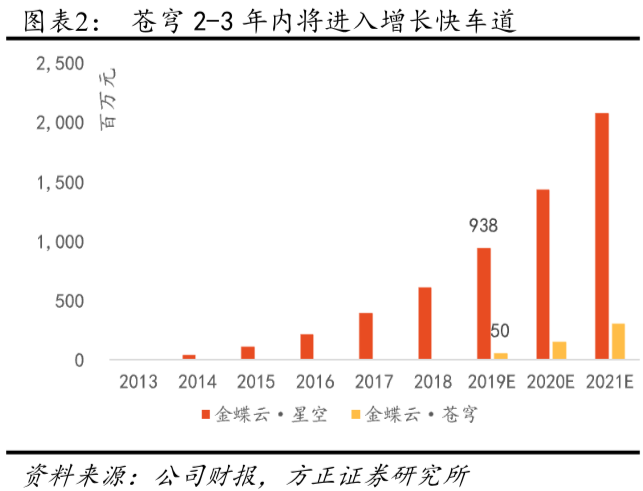

1.云收入维持50+%增长,符合市场预期。全产品线增长,公司云业务继续高歌猛进。一代云·星空仍是增长主要动能,收入3.84亿元,同比增长50.5%,续费率维持90%以上。星空产品架构、销售体系和客户服务均较为完善,随着市场大面积推广,预计未来客户数将继续维持较高速增长。二代云·苍穹客户接踵而至,2 - 3年内有望接力星空。苍穹是国内首个云原生PaaS平台,中国百亿级企业数百家,十亿级企业上千家,在自主可控和企业数字化的趋势下,苍穹未来客户空间巨大。目前,苍穹一年内累计签约客户43家,完善生态和标杆客户项目建设将是当前重点,预计仍有2 - 3年研发投入阶段。

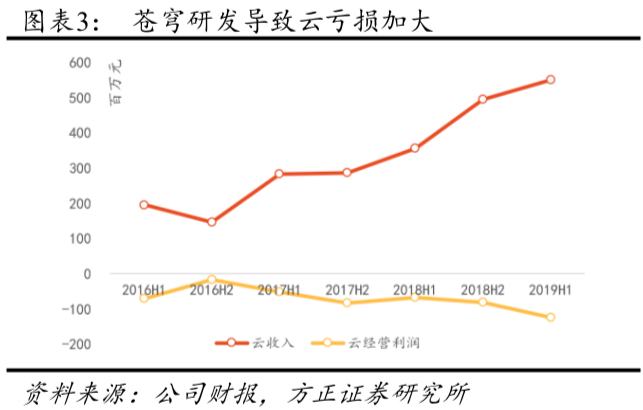

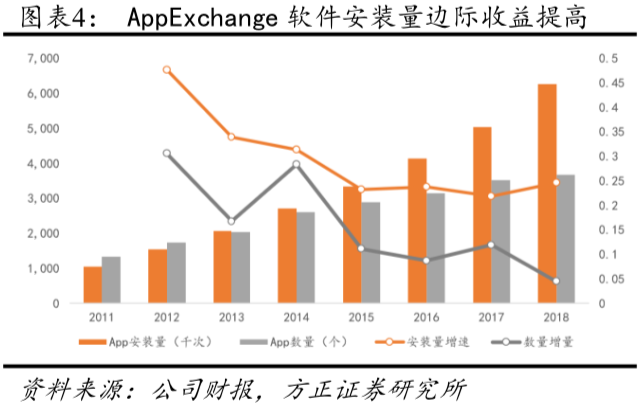

2.星空有望年内盈亏平衡,苍穹仍在建设阶段。云营业利润方面,19H1亏损加大,主要来自苍穹平台的前期研发。我们看好PaaS+ISV的生态,平台搭建完善后,研发费用有望大幅下降,借鉴Salesforce开发AppExchange的经验,软件数量增长会带来客户数量以及单位安装量的边际收益提高。

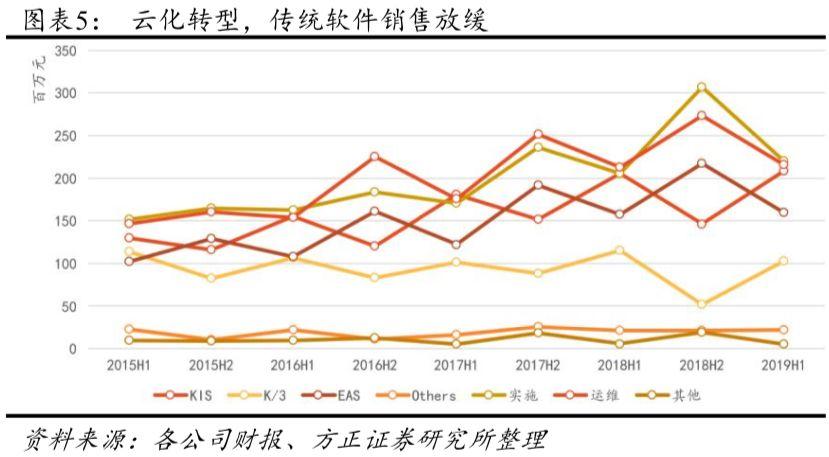

3.传统软件增速下滑,合理化转型。由于传统ERP业务增速下降,我们预计ERP全年增速仍为个位数,影响利润。但传统软件转云,是公司的主要战略和长远目标,市场对此已有充分预期。

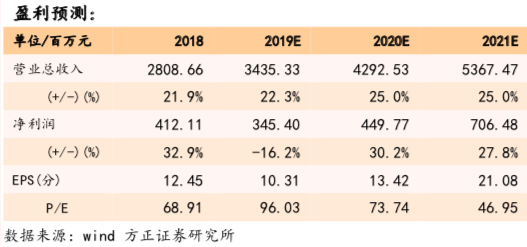

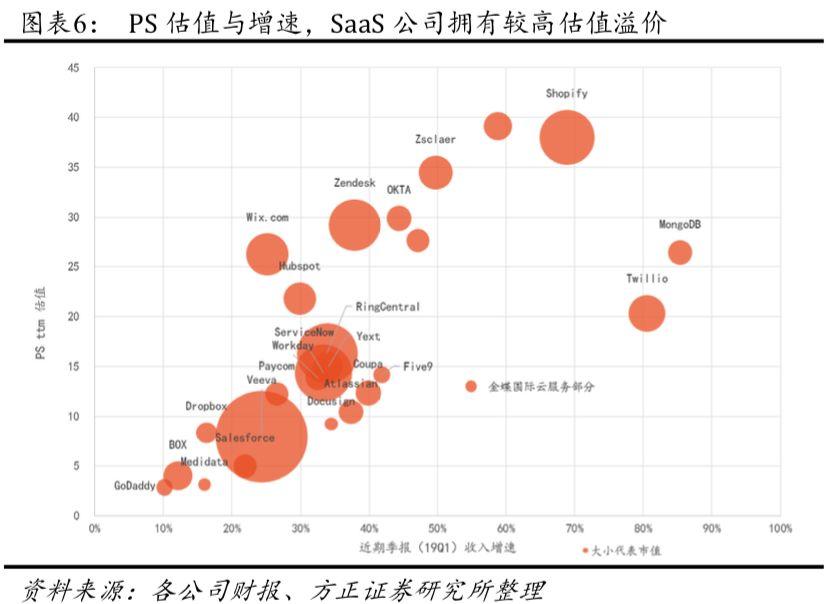

4.投资评级与估值:我们预计公司19/20年营收分别为34.4亿/42.9亿元,EPS为10分/13分。基于分部估值法,给予云业务19年13x PS和ERP业务13x PE,维持目标价HK$ 8.95,仍看好公司长期发展,维持“推荐”评级。对于13x PS估值,我们综合考虑了全球SaaS公司增速与估值,认为金蝶国际作为国内SaaS ERM龙头,目前体量仍有较大发展空间,估值低于大部分美股SaaS公司,较为合理。

风险提示:国内云市场竞争加剧,导致产品毛利率下降;市场需求变化,导致CAPEX和OPEX费用率上升;传统ERP软件市场需求不达预期;国家智能制造推进进度不达预期;金蝶云二代产品不达预期;公司治理及管理人员变动等。

事件:

金蝶国际8月13日发布19H1财报,收入14.85亿元,同比上升16.1%。归母净利润1.10亿元,同比下降35.4%,EPS 3.4分。

点评:

1云收入维持50+%增长,符合市场预期

全产品线增长,公司云业务继续高歌猛进,总体YoY +54.9%。

一代云· 星空仍是收入增长主要动能,收入3.84亿元,同比增长50.5%,续费率维持90%以上。星空产品架构、销售体系和客户服务均较为完善,随着销售体系大面积推广,预计未来客户数将继续维持较高速增长。

二代云· 苍穹客户接踵而至,2 - 3年内有望接力星空。苍穹是国内首个云原生PaaS平台,中国百亿级企业数百家,十亿级企业上千家,在自主可控和企业数字化的趋势下,苍穹未来客户空间巨大。目前苍穹一年内累计签约客户43家,完善生态和标杆客户项目建设将是当前重点,预计仍有2 - 3年投资研发阶段。

星空有望年内盈亏平衡,苍穹仍在建设阶段。云营业利润方面,19H1亏损加大,主要来自苍穹平台的前期研发。我们看好PaaS+ISV的生态,平台搭建完善后研发费用将大幅下降,借鉴Salesforce开发force.com中AppExchange的经验,软件数量增长会带来客户数量以及单位安装量的边际收益。

2传统软件增速下滑,合理化转型

由于传统ERP业务增速下降,我们预计ERP全年增速为个位数,影响利润。但传统软件转云是公司的主要战略和长远目标,市场对此已有充分预期。

3 盈利预测与估值

我们预计公司19/20年营收分别为34.4亿/42.9亿元,EPS为10分/13分。基于分部估值法,给予云业务19年13x PS和ERP业务13x PE,维持目标价HK$ 8.95,仍看好公司长期发展,维持“推荐”评级。

对于13x PS估值,我们综合考虑了全球SaaS公司增速与估值,认为金蝶国际作为国内SaaS ERM龙头,目前体量仍有较大发展空间,估值较为合理。

4风险提示:

国内云市场竞争加剧,导致产品毛利率下降;市场需求变化,导致CAPEX和OPEX费用率上升;传统ERP软件市场需求不达预期;国家智能制造推进进度不达预期;金蝶云二代产品不达预期;公司治理及管理人员变动等

More Content