机构:招银国际

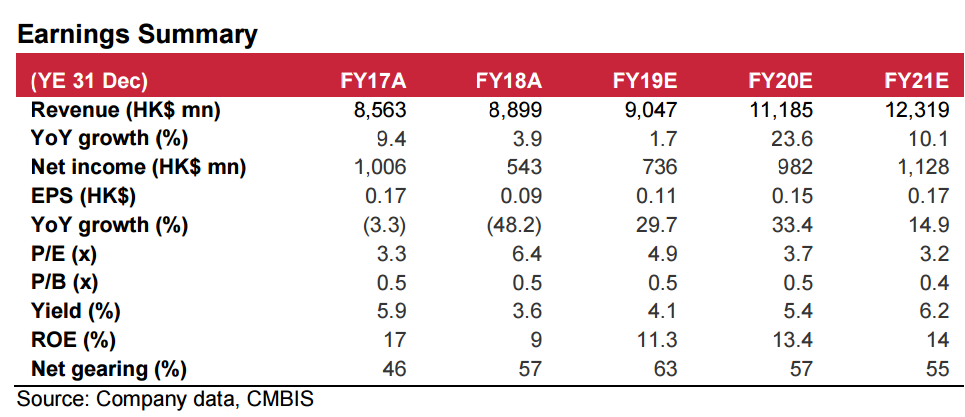

SUMMARY. Tongdas 1H19 weakness with revenue/NP decline of 6%/25% YoY Current Price HK$0.56 was largely anticipated. Net profit was 14% above consensus given better GPM but 13% below our estimates on finance cost. Following NP decline in 2H18/1H19, we estimate strong earnings growth of 240%/33% in 2H19/20E, driven by strong glastic demand from Samsung and improving GPM on low base in 2H18. After hosting HK NDRs yesterday, we are now more confident on earnings recovery, and raised our TP to HK$0.91 (62% upside), based on 6x FY20E P/E (from 5x for better outlook/earnings visibility).

Weak 1H19 expected given metal pressure and biz restructuring. We believe Tongdas weak revenue of -6% YoY is largely in-line, in view of 1) casing segment (73% of sales) decline of 1.3% given sluggish smartphone market, 2) appliances/household & sports segments slumped by 32.3%/8.1% YoY due to biz restructuring, 3) spin-off of notebook biz, and 4) continued GPM pressure on weak metal casing.

Major beneficiary of Glastic casing demand. Mgmt. estimated glastic TAM of 200mn/300-400mn in FY19/20E given rapid adoption from major OEMs (esp. Samsung). As early mover in glastic market, Tongda is poised to become largest glastic supplier for Samsungs mid-end models (A-series) in FY19E. Mgmt. guided 140mn/180-200mn casing shipment in FY19/20E (glastic: 100mn/150mn), driven by Samsungs order win and new client (Vivo) in 2H19E. We estimate glastic revenue to grow 56%/39% in FY19/20E, accounting for 49%/54% of FY19/20E sales.

iPhone share/content growth in 2019; Watch/Airpod order win in 2020. We expect Apple revenue to grow 17%/29% YoY in FY19/20E (19%/20% of sales), backed by 1) content growth in 5G iPhone, 2) penetration into Watch and Airpods, and 2) share gain to 40% in iPhone waterproof (vs 30-35% in FY18).

Earnings turn around in 2H19E; Lifted TP to HK$0.91 (62% upside). We are positive on Tongdas recovery with 30%/33% YoY EPS growth in FY19/ 20E. We adjusted FY19/20/21E NP by -8% /+4%/-1%, and raised our TP by 20% to HK$0.91 based on 6x FY20E P/E (from 5x) given stronger outlook and earnings visibility. Upcoming catalysts include Samsung product launch and China 5G rollout.