本文來自:翠鳥資本

上市公司年報披露已結束,然而,部分業績存有“懸疑”的公司,被“火眼金睛”的交易所密切關注。

貴州百靈(002424.SZ)就是一例。

作為一家知名的中藥企業,貴州百靈2022年的年報有多個“痛點”被指了出來,諸多財務數據透露着不尋常的信號。

與此同時,貴州百靈董事長的股權質押比例不低,這給這家公司基本面披上了不小的陰影。

應收賬款問題多

貴州百靈是一家集苗藥研發、生產、銷售於一體的醫藥上市公司,大眾比較熟悉的產品包括銀丹心腦通軟膠囊、咳速停糖漿維C銀翹片、小兒柴桂退熱顆粒等,這也是該公司的主要盈利產品。

先來看2022年業績。

財報顯示,貴州百靈實現營業收入35.4億元,同比增長13.79%;歸屬於上市公司股東淨利潤1.38億元,同比增長16.64%;扣非後淨利潤8350.95萬元,同比增長5.49%;經營活動產生的現金流量淨額為5.02億元,同比增長54.55%。

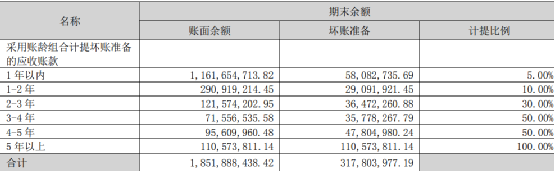

公司主要財務指標同比增幅看似不錯,然而,應收賬款等數據“報警”。

財報有如下一段數據:

應收賬款賬面餘額19.12億元,壞賬準備計提金額3.78億元,壞賬準備計提比例為19.77%。

單項金額重大並單獨計提壞賬準備的應收賬款賬面餘額6018.71萬元,壞賬準備計提比例為100%。

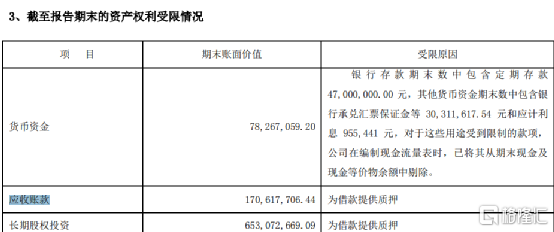

如上圖所示,2022年末貴州百靈有1.7億元的應收賬款處於資產權利受限的狀態,主要為借款提供質押。同期,另有6.53億元的長期股權投資也受限,同樣因為為借款提供質押。

公司還在年報中稱,由於應收賬款金額重大,且應收賬款減值涉及重大管理層判斷,“我們將應收賬款減值確定為關鍵審計事項”。

細分來看,應收賬款的壞賬準備提及比例最高的部分,主要集中於3-4年、4-5年及5年以上的應收賬款。

比如,無法收回並核銷的應收賬款中,有一筆涉及鄭州邦正醫藥有限公司等多家零星小額單位合計的貸款,核銷金額達到1035萬元。

多項指標落後

貴州百靈的財務指標,一旦和同行業公司比較的話,很多劣勢都出現了。

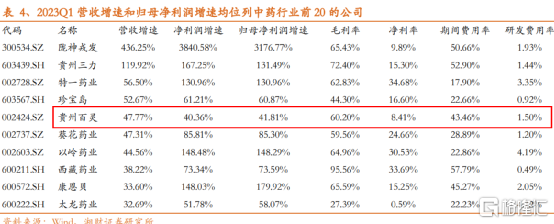

以2023年一季度營收增速為例,貴州百靈錄得的增速是47.77%,大幅落後於多家重要行業公司,諸如隴神戎發、貴州三力、特一藥業和珍寶島。

實際上從上圖可以看出,如果説貴州百靈的上述營收增速勉強夠“撐場”的話,那麼淨利潤增速、歸母淨利潤增速以及淨利率就可以説是墊底的了。

再以2022年業績為例,74家中藥上市公司中,貴州百靈的年度歸母淨利潤為例第39位。

雖然處於行業中游的位置,但差距卻相當大。全行業至少有8家公司歸母淨利潤超過10億元,最頭部的六家公司均超20億元,但同期貴州百靈僅僅邁過億元大關。

實控人質押比例高

數據顯示,貴州百靈董事長姜偉目前持有公司2.45億股股份,佔公司總股本的17.39%,其中83.49%處於質押狀態。

最新一場機構投資者的調研活動中,買方機構十分關注這個問題。

貴州百靈現場給出了“避重就輕”的解答。

其稱,姜偉現股份質押融資用途為投資運營的非上市公司產業及償還其股票質押式回購交易負債,不用於滿足上市公司生產經營相關需求,其質押的股份不負擔業績補償義務。

上述重點內容是非上市公司產業,而非上市公司生產經營。

公司高管進一步稱,姜偉負債總額已得到大幅度降低,資信狀況良好,具備相應的資金償還能力,目前不存在平倉風險或被強制平倉的情形,後續如出現平倉風險,將採取提前購回、補充質押等措施進行應對。

而事情並沒有這麼簡單。

2022年12月末,貴州百靈的實控人經歷過一場變動。

當時,身為控股股東、實際控制人姜偉及其一致行動人姜勇,手中分別持有的1020萬股和5407.12萬股貴州百靈遭拍賣,成交價格近6億元。

正是這次事件之後,貴州百靈的實際控制人由姜偉、姜勇變更為“單一人物”姜偉。自此,姜勇直接出局。

梳理公吿發現,自2019年初以來,姜氏家族多次通過協議轉讓,變相減持上市公司股票的方式,償還股權質押借款。更有統計數據顯示,貴州百靈上市以來累計發佈超過300條的質押相關的公吿。

資料顯示,姜偉屬於中藥專業人士,他幼年時代隨父母支援三線建設來到貴州安順雲馬飛機制造廠。

1982年姜偉畢業於貴陽中醫學院藥學系,1996年10月,原貴州省安順製藥廠以產權整體轉讓給安順宏偉實力有限責任公司,實現國有資產流動與重組,姜偉任董事長兼總經理。2003年6月安順製藥廠正式更名為貴州百靈製藥有限公司,並於2010年6月實現IPO。

姜偉的這場資本局究竟是為了什麼?上市公司對其質押問題的最新解釋,能否站得住腳?

這直接關係到諸多中小股東的利益。

※此文為翠鳥資本原創文章,未獲授權請勿轉載。

More Content