港股配置比例明顯高於同行。

千億級私募機構的「投資佈局」,從來都是謹慎、更謹慎,意外、真意外!

資事堂獲悉:截至今年9月末,景林資產旗下的FOF(組合基金)的港股資產佔總倉位接近50%,這個比例超過了該基金組合內的A股資產(後者佔約三成比例)。

如此「重金押注」一個離岸市場,在中國國內私募圈可謂相當「罕見」和「剛猛」。

而這也從另一個角度註釋了「景林」的投資風格:一旦認準機會,毫不動搖, 「兩個腳都要踩上去」抓機會。

配置比例曝光

根據資料,景林資產的FOF產品平均投向旗下多個獨立運作的私募基金,涵蓋景林最有代表性的四位基金經理——蔣錦志、蔣彤、金美橋、高雲程。

而這隻未被關注的FOF產品,則成爲了這家千億私募的「投資晴雨表」。

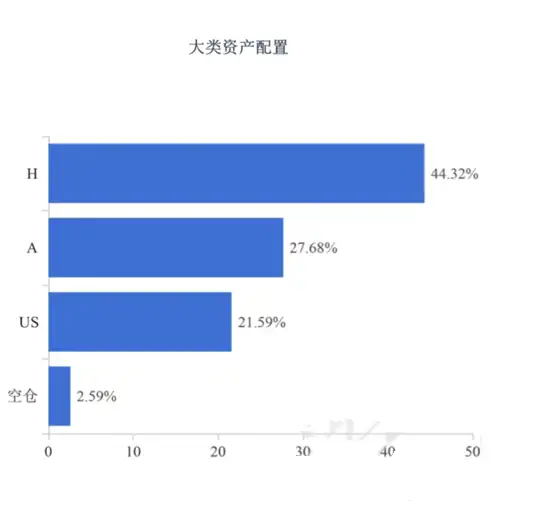

根據最新的景林FOF月報顯示:該基金目前最新的大類資產配置比例依次爲H股(佔比44.32%)、A股(佔比27.68%)、美股(佔比21.59%)。

H股和A股資產佔比遙遙領先。

持續增持港股

上述組合的信息截至今年9月末,對比7月末,景林的港股配置增長了近6個百分點。

這足以看出景林資產對港股市場的「重視」。

景林資產在月報中說道:「港股目前估值極度便宜,我們認爲上漲空間很可能大於下跌風險,風險調整後收益已極具吸引力。」

對於「便宜」的證據,景林資產進一步指出:9月港股股票回購規模達到176億港元,刷新有史以來月度最高紀錄。歷史上來看,股票回購規模的大幅增長在中期通常是市場觸底的信號,目前港股估值已經極度便宜。

錨定「科技」與「消費」

景林的賽道佈局依然是它們自身最擅長、賺錢較多的消費板塊和科技板塊。

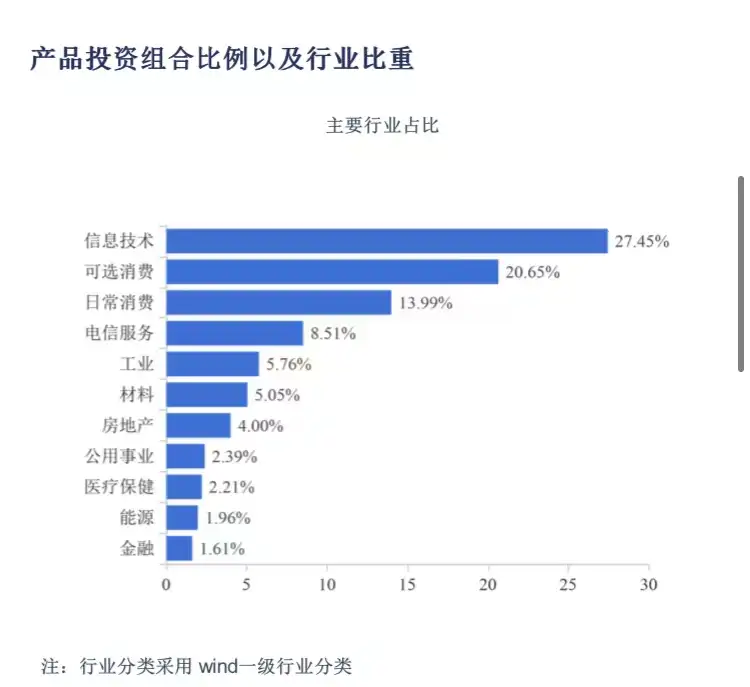

公告顯示,景林FOF的前五大行業配置分別爲信息技術(佔比27.45%)、可選消費(佔比20.65%)、日常消費(13.99%)、電信服務(8.51%)、工業(5.76%)。

大TMT和消費依然是最重要配置,配置比例均超過30個百分點。

互聯網大廠或成重點之一

那麼行業以下,景林配置的重點品種可能包括哪些品種?

此前景林資產曾在路演中提及:未來看好包括互動娛樂、新零售和新服務平臺、新能源結構下的應用、深度數字化軟硬件、人工智能的發展和應用、社交屬性的消費品。

這段描述非常各專業,但是從社交屬性、新零售、互動娛樂、新服務平臺等措辭推測,一些港股上市的互聯網平臺企業可能有這個特點。

景林當時還指出:我們更加確定地觀察到零售、生活服務的線上化趨勢繼續加強,平臺公司成爲了商業服務和流通領域的基礎設施。互聯網平臺公司處於業績底+政策底+估值底的三底疊加狀態,去年下半年開始的低基數效應會讓大部分公司重回增長正軌。

景林資產投向的美股資產中,也主要覆蓋此類企業, 以二季度末的投資數據爲例,景林持有京東集團、網易、阿裏巴巴、中通快遞、拼多多等消費互聯網公司。

誰主導了港股加倉?

景林FOF是這家機構2021年發行的產品,投向蔣錦志、蔣彤、金美橋、高雲程四位基金經理管理的產品。

因此,接近半數的港股配置比例,是上述基金經理產品穿透後的平均數值。

資事堂瞭解到:高雲程曾在路演中透露今年以來股票配置切換爲50%中國公司、50%的非中國公司,以此分散國別配置風險。

蔣彤曾參與過港股新股的投資(比如泡泡瑪特等),蔣錦志和金美橋長期在海外進行投研,因此對離岸市場有較高關注度。

再來看FOF業績。

以今年9月份爲例,這隻FOF淨值跌幅爲11.4%,與恆生指數跌幅相當。

此外,該產品年內收益-18.98%,好於同期滬深300和恆生指數跌幅分別爲-24.34%、-26.08%。

信心超乎同行

資事堂注意到,儘管景林FOF以接近一半的倉位佈局港股,但這樣的持倉路數在中國內地同行中並不多見。

同樣管理千億資產的淡水泉爲例,代表產品的港股配置比例是15%左右,其他均爲A股資產。

另據瞭解,多數百億私募的主觀多頭產品,其港股配置普遍在10%-30%區間。

一些國內私募管理坦誠,目前的組合配置還是以「A股+H股」的模式爲主,這主要考慮到以下因素:

1、部分基金經理認爲,港股的資金結構和波動特點和A股不同,港股的底層資金中,海外投資者佔據相當比例,對境內機構而言存在一定投研難度。

2、近兩年熱門賽道新能源相關的產業鏈上下遊公司,多集中於A股。港股的特點是網絡經濟和生物醫藥,後者近期景氣度有爭議。

3、承認港股估值不斷牀下新低,但也認爲,估值低屬於行情的充分非必要條件。

而景林成立時間非常早,且很早就探索海外市場的投資,對離岸市場的熟悉程度。可能是它們敢於大幅加倉的理由。

More Content