中信證券:7月非農就業薪資雙強,聯儲鷹派難改

本文來自格隆匯專欄:中信證券研究 作者:崔嶸

核心觀點

7月美國非農新增就業人數遠高於市場預期,教育和保健服務、休閒和酒店業以及專業和商業服務貢獻了主要新增就業人數。美國就業市場已基本恢復至疫情前水平,同時薪資增速超預期走高,增加工資-價格螺旋風險。當前,衰退擔憂再次轉向通脹擔憂,美聯儲鷹派立場短期難改。9月加息幅度仍取決於更多數據,預計市場將在波動中尋找平衡,美元指數仍有支撐,美股仍是熊市中的反彈。

事項

美國2022年7月新增非農就業人數52.8萬(預期25萬,前值39.8萬);失業率為3.5%(預期3.6%,前值3.6%);平均時薪同比增長5.2%,環比增長0.5%(預期分別為4.9%和0.3%);勞動參與率為62.1%(預期62.2%,前值62.2%)。

正文

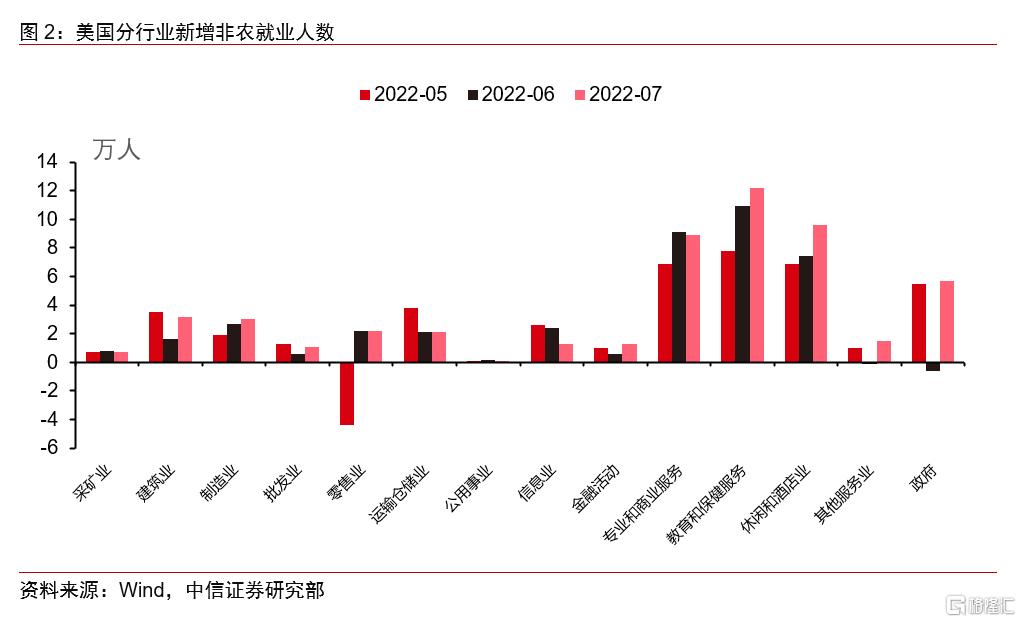

▌ 7月美國非農新增就業人數遠高於市場預期,教育和保健服務、休閒和酒店業以及專業和商業服務貢獻了主要新增就業人數。總體來看,7月美國非農新增就業人數為52.8萬人,為2022年2月以來單月最高值,遠超市場預期的25萬人。6月數據從37.2萬上修至39.8萬,同時5月數據從38.4萬上修至38.6萬。7月失業率為3.5%,優於市場預期的3.6%及前值3.6%。分行業來看,商品生產類別中,建築業、製造業新增就業人數均有所回暖,分別從1.6萬上升至3.2萬,2.7萬上升至3萬。服務類別中,教育和保健服務、休閒和酒店業以及專業和商業服務貢獻了主要新增就業人數,分別增加12.2萬人、9.6萬人和8.9萬人。政府部門新增就業5.7萬人,遠超前值的-0.6萬人。

▌ 美國就業市場超預期強勁,已基本恢復至疫情前水平,同時薪資增速超預期走高,增加工資-價格螺旋風險。一方面,從7月新增非農就業人數和失業率來看,當前非農就業總人數已經恢復至疫情前水平,其中,私人部門就業人數比2020年2月增加62.9萬人,而政府部分就業人數則仍比2020年2月減少59.7萬人;同時,失業率進一步走低至3.5%,與2020年2月持平,顯示美國勞動力市場仍然強勁。勞動參與率繼續小幅下降或與美國新冠確診病例增加以及猴痘確診病例增加有關。另一方面,此前有所回落的平均時薪增速在本月再次抬頭,使工資-價格螺旋上升的風險有所抬升,同時由於薪資增速和美國CPI中的核心服務相關性較強,因此也進一步加大了聯儲抗擊通脹的壓力。

▌ 衰退擔憂再次轉向通脹擔憂,美聯儲鷹派立場短期難改。在7月非農數據公佈前,由於鮑威爾在7月議息會議上釋放“有條件的鴿聲”(詳見《美聯儲2022年7月議息會議點評:有條件的鴿聲》,2022-07-28)以及美國經濟進入“技術性衰退”(詳見《2022年第二季度美國GDP增速點評:“技術性衰退”已來,“實質性衰退”漸近》,2022-07-29),市場預期美聯儲貨幣政策收緊將在衰退擔憂下轉向緩和。但本週多位聯儲官員講話一致釋放鷹派信號,表明市場低估了美聯儲加息抗擊通脹的決心。在強勁的就業和薪資增速數據公佈後,短期而言,市場對於衰退的擔憂或將再次轉向對通脹的擔憂,結合我們對下週將要公佈的美國7月CPI數據仍將維持在8.8%左右高位的判斷,預計美聯儲鷹派立場短期難以出現明顯改變。

▌ 9月加息幅度仍取決於更多數據,預計市場將在波動中尋找平衡,美元指數仍有支撐,美股仍是熊市中的反彈。由於美聯儲9月議息會議前仍有諸如7月CPI、8月非農和CPI等多項數據披露,而當前美聯儲主要基於實際數據來進行相機抉擇,因此9月加息50bps還是75bps當前尚無定論。預計衰退預期和通脹預期仍將反覆輪動,加息預期也將繼續波動,而市場仍將在波動中尋找平衡。就美元指數而言,無論是美聯儲相對歐央行和英國央行的加息步伐,還是美國相對歐元區和英國的經濟基本面,均對美元指數仍有支撐,預計美元指數年內仍將在110以內磨頂。就美股而言,儘管在美聯儲轉向預期的影響下美股出現階段性反彈,但我們預計美聯儲加息進程可能超出市場預期,同時本輪美國通脹或只能通過經濟衰退來緩解,因此,市場或仍未充分定價美聯儲加息路徑,同時部分行業將面臨盈利下修風險,美股當前或仍是熊市中的反彈。

▌ 風險因素:美國通脹超預期回落;美國經濟超預期在年內進入實質性衰退。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.