本文來自:中國宏觀經濟論壇 CMF,作者:王晉斌

美國金融市場條件已經快速收緊,流動性依然充裕。風險溢價並未顯著提高,表明投資者風險偏好並未出現明顯惡化,國債收益率期限溢價的快速收窄,甚至倒掛,使得金融市場出現了緊縮貨幣所致經濟衰退的弱信號。流動性充裕、風險偏好沒有明顯惡化和部分倒掛的收益率曲線使得美國金融市場信號進入難以識別期,投資者可能會沒有方向感,在多種因素的共同作用下,信號難以識別期或將持續。

在貨幣政策緊縮預期的引導下,至今美聯儲僅加息25個基點,從3月17日開始美聯儲聯邦基金利率上調至0.33%(0.25%+0.08%),美國金融市場的金融條件指數已經超過疫情前水平,金融市場運行環境相對疫情前已經有所收緊;儘管金融市場流動性依然充裕,而風險溢價基本恢復到疫情前的水平。只有足夠投資者風險偏好支撐,未來風險資產價格才能避免出現較大級別調整的風險。

截至2022年3月11日的一週,美國金融條件指數為-0.35082,已經超過疫情前水平。尤其是今年以來,從年初的-0.60614出現了快速上升。今年年初的金融條件水平與疫情前2020年初的水平大致相當,目前的金融條件指數已經明顯高於2016-2019年的水平。因此,此輪美國經濟中寬鬆的金融條件基本已經結束(圖1)。

圖1、美國經濟中的金融條件指數

數據來源:Federal Reserve Bank of St. Louis, Chicago Fed National Financial Conditions Index, Index, Weekly, Not Seasonally Adjusted.

從金融市場流動性來看,紐約聯儲3月23日逆回購規模高達1.803萬億美元,處於歷史第二高位,僅次於2021年12月31日1.905萬億美元的歷史最高水平。今年以來,紐約聯儲的逆回購規模基本保持在1.5萬億美元以上,美國金融市場的流動性是充裕的。

從風險溢價情況來看,整個金融市場風險溢價水平已經恢復到疫情前水平。依據美聯儲聖路易斯分行的數據,從美國高收益指數期權調整利差來看,截至2022年3月22日為3.70%,低於疫情前2018-2019年兩年的日均3.85%和2019年的日均4.01%;但考慮到3月15日曾達到今年以來的高點4.21%,因此,可以認為高收益債券的風險溢價水平與疫情前相比相差不大。美國金融市場高風險的溢價水平比歐元區要低。3月22日歐元區高收益指數期權調整利差4.22%,要明顯高於疫情前2018-2019年兩年的日均3.66%和2019年的日均3.84%,一個重要原因是俄烏軍事衝突推高了歐元的風險溢價水平。

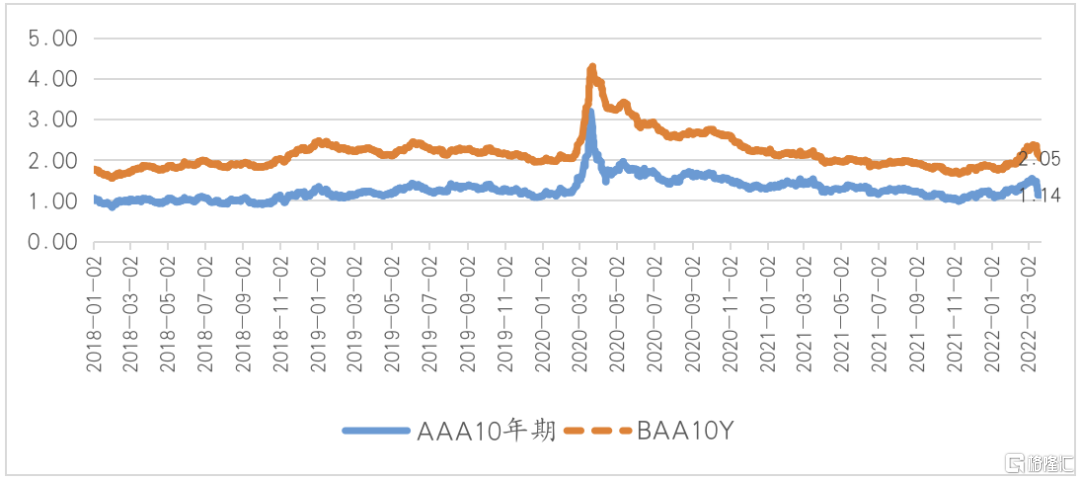

從穆迪Aaa和Baa公司債券的風險溢價水平來看,今年以來也出現了一些變化。今年年初,穆迪Aaa和Baa公司債券的風險溢價水平分別為1.16%和1.82%,3月22日兩者分別為1.14%和2.14%。在3月中旬開始,兩者出現了一個明顯的下降,主要原因可能是俄烏衝突談判帶來了風險溢價水平的下降。

圖2、穆迪不同級別債券的風險溢價水平(%)

數據來源:Federal Reserve Bank of St. Louis, Moody's Seasoned Aaa and Baa Corporate Bond Yield Relative to Yield on 10-Year Treasury Constant Maturity, Percent, Daily, Not Seasonally Adjusted.

從美國國債市場的收益率來看,美國國債市場已經對美聯儲的緊縮預期產生了強烈的反應,甚至存在過度反應的傾向。依據美國財政部網站公佈的數據,10年期美國國債收益率從年初的1.63%上升至3月23日的2.32%,上漲了69個BP;2年期美國國債收益率從年初的0.78%上升至3月23日的2.13%,上漲了135個BP;1年期美國國債收益率從年初的0.40%上升至3月23日的1.52%,上漲了112個BP;美國國債長短期利差出現了急劇的收窄,5年期、7年期國債與10年期國債收益率出現了倒掛,以至於市場出現了美聯儲加息會導致美國經濟衰退的預期信號。

目前美國金融市場信號進入了這種難以識別的時期,這是多種因素共同作用的結果。首先,美聯儲控通脹的速度和力度是否會引發美國經濟失速,市場出現這種擔心是正常的;其次,俄烏軍事衝突何時結束,戰爭風險溢價的估值市場也很難給出判斷;再次,全球疫情依然具有不確定性,那麼對全球供應鏈的衝擊也具有不確定性。

在這樣的背景下,金融市場投資者可能會沒有方向感,其行為表現出來的各種價格信號也因此進入難以識別期,這種信號難以識別期可能會持續一段時間。

More Content