懶理隔夜美股暴跌,港股虎年發威了!恆指飆漲750點,科技、汽車股狂拉!阿里市值大增1200億港元

懶理隔夜美股暴跌,港股在虎年首個交易日雄起了!

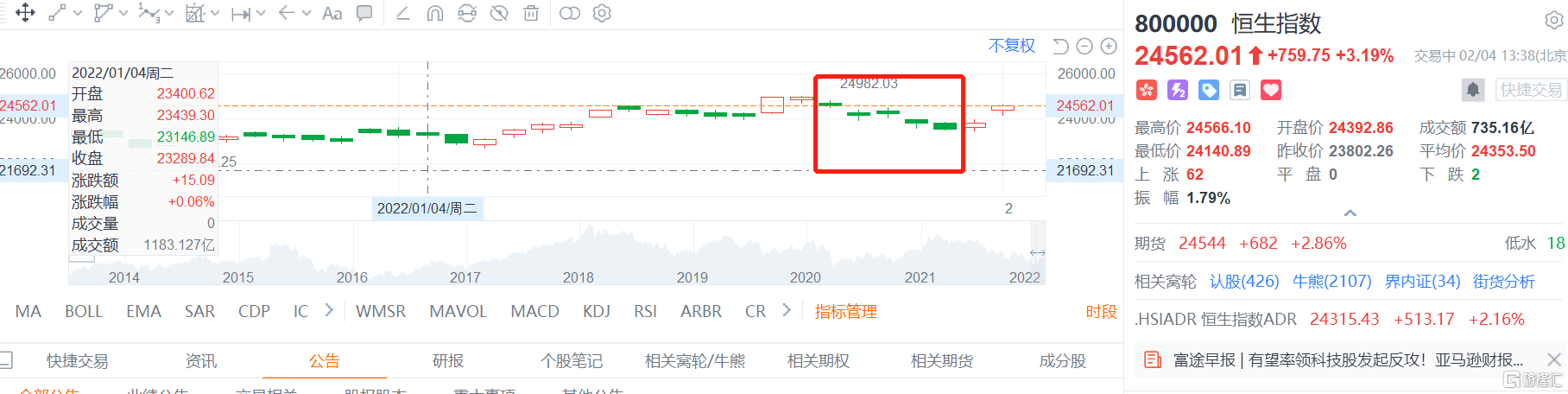

2月4日,大年初四,恰逢立春,港股虎年首個交易日開門紅,三大指數高開高走,恆指午盤漲2.71%,恆生科技指數漲2.29%。午後開盤,港股攻勢更猛,截止發稿,恆指飆漲3.16%,報24553.71點,大漲751點。

其中汽車板塊表現強勢。理想汽車漲超12%,小鵬漲超10%,比亞迪漲超7%。

消息面上,造車新勢力“理小蔚”近日紛紛發佈1月交付數據。其中,蔚來2022年1月交付新車9652台,同比增長33.6%;小鵬汽車1月交付12922輛,同比上漲115%,歷史累計交付量超過15萬輛;理想汽車1月共交付12268輛理想ONE,同比增長128.1%,且連續3個月交付破萬。

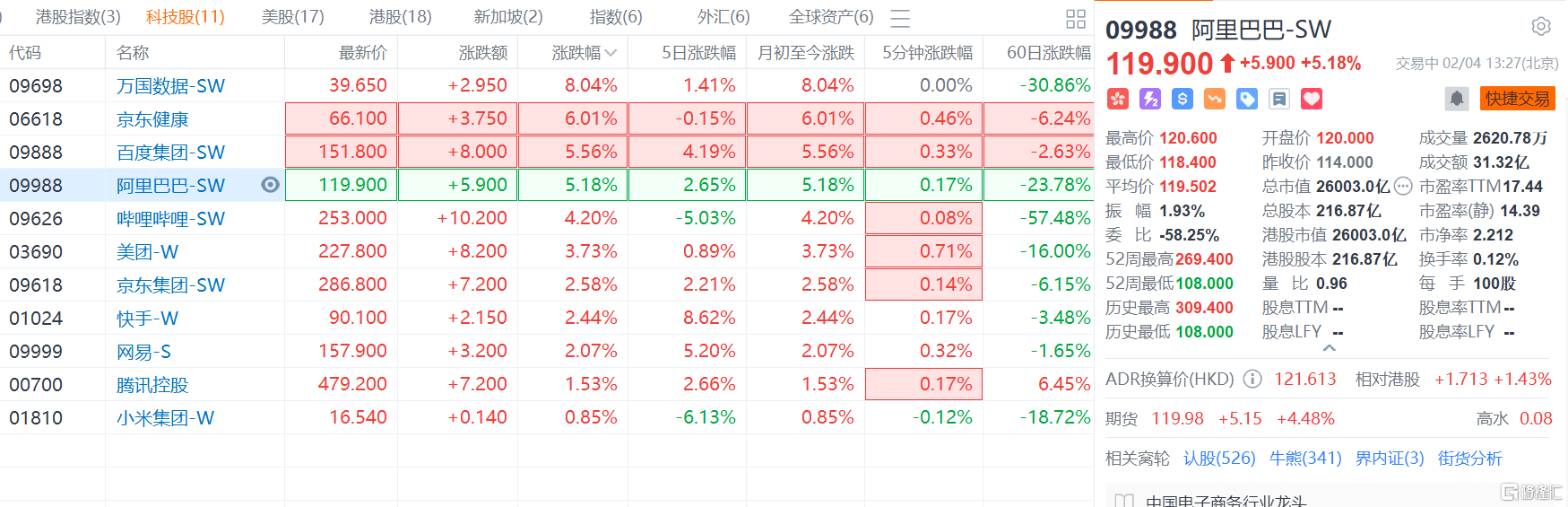

互聯網科技股的漲幅也不甘落後。萬國數據漲超8%,京東健康漲超6%,阿里漲超5%,市值飆漲1279億港元至26024億港元。嗶哩嗶哩漲超4%,美團漲超3%。

但值得注意的一點是,隔夜美股上演黑色大風暴。在Meta財報“暴雷”和全球主要央行加速收緊貨幣政策的影響下,美股三大指數週四集體低開低走,大幅收跌,納指跌3.74%,標普500指數跌2.44%,道指跌1.45%。納斯達克100指數暴跌4.2%,為2020年9月以來最大跌幅。

美國科技股普遍重挫,其中Meta Platforms收盤跌26%,也創下單日市值蒸發2375億美元的歷史新紀錄。蘋果跌1.67%、特斯拉跌1.60%、亞馬遜跌7.81%、谷歌A跌3.32%、奈飛跌5.56%、微軟跌3.90%、高通跌4.84%、AMD跌2.18%、英偉達跌5.13%。

在2021年熊冠全球的港股為何在虎年首個交易日如此強勢?

事實上,在農曆春節前,港股的反彈遭遇黑色四連陰。

這主要是基於當時臨近美聯儲2022年第一個議息會議,鑑於在去年12月FOMC會議至今不到兩個月的時間裏,美聯儲的政策取向發生了劇烈的轉變,拋棄了此前“通脹只是暫時性”的觀點。市場的擔憂明顯提升,對今年加息的預期也從1-2次大幅飆升至4次,甚至擔憂一次性加息50bps。

美聯儲預計3月初結束Taper,並暗示3月加息符合市場預期,啟動加息進程後開始縮表。聯儲主席鮑威爾表示聯儲有充足空間在不危害經濟增長的情況下加息,強化為打壓高通脹不惜一系列加息的態度,且不排除聯儲每次會議都加息的可能,需要大規模縮表,至少加息一次後開始討論縮表。

FOMC 1月利率決議會議靴子落地後,金融市場開始趨穩。

此外,當時地緣政治局勢顯著升温,俄羅斯及烏克蘭和北約部隊均在邊境開展軍演,大規模衝突的風險一觸即發,全球資產劇烈波動。港股作為典型的離岸市場,也不可避免地受到了波及。

不過目前俄烏局勢暫時有趨穩的現象。當地時間1月26日,為緩解當前烏克蘭危機,法國、德國、俄羅斯、烏克蘭在法國巴黎共同舉行“諾曼底模式”四方會談,就緩和烏克蘭危機等問題展開磋商四方在會談後表示,各方應無條件遵守停火協議,並加快推進明斯克協議的實施。

春節前,受制於三大經濟下行壓力,A股更是跌跌不休,創業板指年初至今跌超12%,也對港股的走勢產生了壓制。

所以,廣發香港分析師鄭新煌認為,港股的這一輪反彈卻顯得有些“時運不濟”,剛剛進入信心修復的蓄勢期,就被外圍市場與在岸市場的接連下挫“攔腰斬斷”。

不過,他進一步表示,目前港股整體的基本面條件並未出現惡化,經濟/盈利下行和美聯儲收水的壓力已經在預期中有相當程度的計入,此前受到壓制的地產、科網等領域的政策甚至還在邊際改善,港股將在科網股和內房股的帶領下迎來一波規模較大的反彈。但港股重新蓄勢的過程則可能需要等到春節過後,操作上需要保持一定的耐心。

興業證券全球首席策略分析師張憶東認為,中國港股2022年對於美股的動盪將逐步脱敏,有望迎來海外資金從其他新興市場迴歸,維持2022年“港股反彈小牛市”的判斷。港股作為“全球估值窪地”,基於中國穩經濟的貨幣政策、財政政策發力以及中國房地產、互聯網等產業政策環境邊際改善,2022年港股將迎來內資和外資增持意願的雙重提升。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.