估值漂移,敏华控股(1999.HK)还有多少上涨空间?

公司以代工软体家居业务起家,后来孵化自有品牌芝华士,成为全球功能沙发的领先品牌,目前在国内市场的市占率高达50%。敏华的这一波上涨,不仅仅因为业绩出色,同时估值已经发生了根本性切换,从制造业公司转变为消费品企业。

从代工龙头走向品牌化

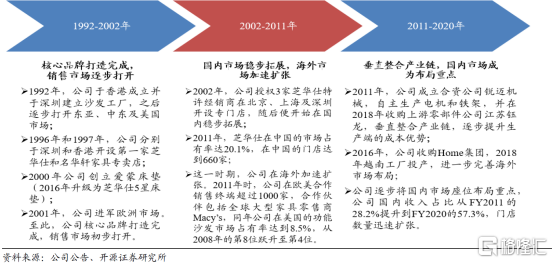

敏华的发展大致可以分为三个阶段:

第一阶段:1992年,公司在香港成立并于深圳建立沙发工厂,之后逐步打开东亚、中东及美国市场。1996 年和1997 年,公司分别于深圳和香港开设第一家芝华仕和名华轩家具专卖店。

第二阶段:2002 年,公司授权3 家芝华仕特许经销商在北京、上海及深圳开设专门店,随后开始在国内市场稳步拓展。2011 年,芝华仕在中国的功能沙发市占率达20.1%,在中国的门店达到660 家。同时这一时期,公司在海外加速扩张。2011 年时,公司在欧美合作销售终端超过1000 家。

第三阶段:2011 年,公司成立合资公司锐迈机械,自主生产电机和铁架,并在2018 年收购上游零部件公司江苏钰龙,垂直整合产业链,逐步提升生产端的成本优势。

在业务拓展上,2016 年,公司收购Home 集团,2018 年越南工厂投产,进一步完善海外市场布局。另一方面,公司逐步将国内市场作为布局重点,公司国内收入占比从FY2011的28.2%提升到FY2020 的57.3%,门店数量迅速扩张。

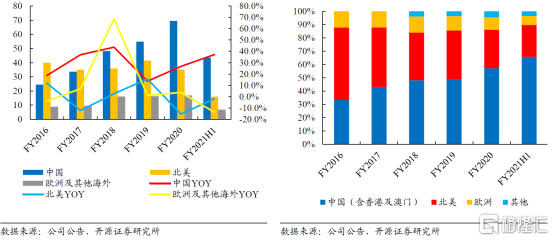

分市场来看,2020年公司在中国市场收入为为69.6 亿港元(+26.7%),占比57.3%,;在北美市场的收入为35.1 亿港元(-15.4%),占比28.9%;欧洲及其他海外市场收入为16.8 亿港元(+3.8%),占比13.9%。

其中中国市场为主要市场,收入从2015年20.7亿港元提高到2020年的69.6亿港元,收入占比从31.5%提升到57.3%。

公司旗下芝华仕品牌在中国功能沙发的市场市占率达50.1%,属于绝对龙头。并且,公司在内销市场正在加速开店以抢占市场份额。截至2020 年9 月30 日,公司拥有线下门店3532 家,对比2020 财年末净增加658 家门店,并且在未来两到三年内仍有望保持较快的开店速度。

竣工回暖下的景气周期

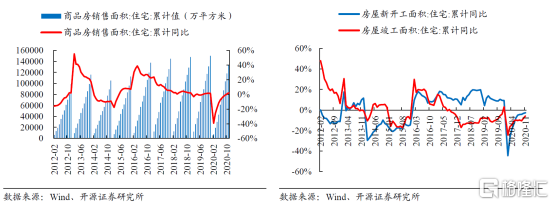

通常来看,从新开工到交房的周期一般不会超过3 年,因此2017 年至今的竣工缺口已经接近亟待回补的临界点。所以,虽然受疫情影响,竣工回补的结点又有所推迟,但我们认为在疫情影响趋弱后,竣工数据已经逐步修复,尤其是2020 年10-11 月竣工回暖的数据已经有所加快。

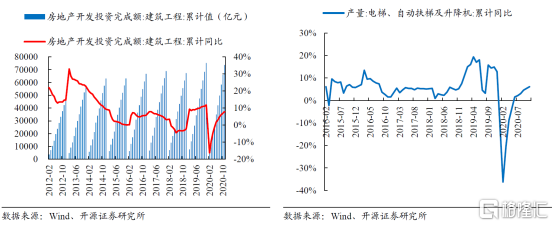

2019 年建筑工程投资额、电梯以及平板玻璃产量等竣工前瞻指标累计同比均处于近年高位,对竣工回暖的预期提供了一定支撑。

2019 年1-12 月,建筑工程投资完成额、电梯产量和平板玻璃产量分别同比增长11.8%、12.8%和6.6%。最终反映到竣工数据上,我们也可以看到2019H2 竣工数据快速修复,并且全年竣工累计同比最终转正。

而2020 年虽然受到疫情冲击,但交房的前瞻指标相比直接的竣工数据也展现了更快的修复速度。2020 年1-11 月,建筑工程投资完成额和电梯产量分别累计同比增长7.9%和6.1%。

敏华的成长得益于短期内快速开店红利,长期来看,同时受益于功能沙发市场集中度的提升和竣工周期的回暖。当前公司的估值已经在向消费品公司切换,对应2021年估值28倍,2022年估值23倍;作为具有品牌消费类属性的公司来说,估值方面有明显优势。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.