銀行角度看12月社融:非標和年底因素擾動,銀行年初項目儲備較多,維持“增持”評級

機構:中泰證券

評級:增持

投資要點

12月社融新增1.7萬億,新增量較去年同期下降3830億。存量社融同比增速環比下降0.29個百分點至13.3%,降幅略超預期。結構分析:12月社融增速低於預期主要為信託貸款和未貼現銀行承兑匯票回落幅度較大:新增信託的收縮在預期內,12月到期規模較大。未貼現銀行承兑匯票預計部分在表內轉貼現以衝信貸額度,考慮全年新增信貸規模已經較大,12月部分信貸項目儲備留存到年初投放亦合理,無需過分擔憂銀行信貸項目儲備不足。正向支撐因素:信貸保持平穩增長;政府債券對社融的支撐超預期,部分對沖了非標的收縮。

12月新增信貸投放規模基本符合預期。12月新增貸款1.26萬億元,市場預期1.21萬億元,較去年同期增加1200億元。信貸餘額同比增長12.8個點,在高位環比持平。結構分析:票據成為支撐主力,其次為企業中長期。居民消費貸和按揭信貸需求有所回落。1、票據高增一定程度也對企業短貸有所替代,在一定的信貸總額度下,企業短貸規模有較大幅度的回落;企業中長期信貸則是基礎設施建設的持續發力。企業短期貸款、票據融資、中長期貸款分別新增-3097億、3341億、5500億,增量較去年同期變動-3132億、+3079億、+1522億元。2、12月居民加槓桿力度有所回落,預計部分按揭類貸款也被留置年初發放。居民短貸、按揭貸款淨新增分別為1142億、4392億元,較去年同期下降493億元、432億元。

M1同比增速略放緩,或與二三線地產銷售回落、新增信託規模大幅下降有關:12月M0、M1、M2分別同比增長9.2%、8.6%、10.1%、較上月同比增速變動-1.1、-1.4、-0.6個百分點。

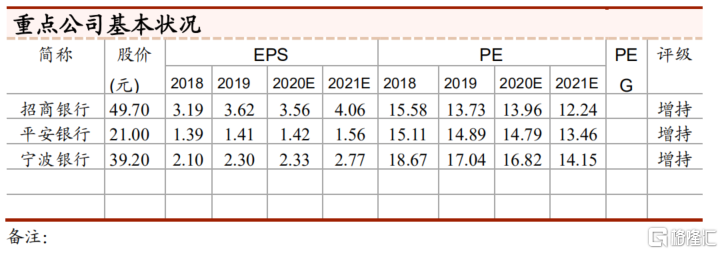

銀行投資建議:銀行股的核心投資邏輯是宏觀經濟,繼續看好板塊估值修復行情。1、我們8月初轉看多銀行,繼續看好伴隨經濟修復帶來的銀行股估值修復行情。本輪銀行股核心邏輯是宏觀經濟,宏觀經濟修復程度決定了銀行股的上漲空間。目前經濟處於上升期,銀行基本面穩健、估值和公募基金倉位在歷史低位,我們判斷銀行估值修復行情會持續。2、個股建議:重點推薦、中長期看好的是優質的銀行:寧波銀行、招商銀行、平安銀行和興業銀行。

風險提示事件:經濟下滑超預期。疫情影響超預期。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.