作者 | Lampredotto

數據支持 | 勾股大數據

七月初的大漲,讓市場上一時充斥了對牛市的討論。但這場"牛市"似乎並沒有持續太久,上上週的三根陰線直接讓很多人改變了對牛市的信仰。

回顧A股歷史,全面性牛市屈指可數,但結構性牛市卻並不罕見,比如17年的漂亮50,這兩年的創業板。實際上,回過頭看,基本上每年都有結構性的機會,就算是"萬馬齊喑"的2018年,油氣板塊也是上漲的。

所以,在大A股市場上,α的機會可能比β的機會更多。當你還在等待牛市的時候,其實很多股票的牛市早就已經開始了。

這麼説來,中公教育的"牛市"從它借殼上市之時,就已經開始了。2019年2月21日,亞夏汽車正式更名為中公教育,完成了借殼上市。此後,中公教育便一路上漲,從9.78塊上漲至昨日收盤的31.2塊,不到一年半時間就漲了219%。

上漲是戴維斯雙擊的結果。這一年半時間,中公教育的估值PE-TTM從64提升至106倍,2019年的歸母淨利潤則增長了56.5%。進入2020年,疫情也絲毫沒有打亂上漲的節奏,只不過上漲的因素更多的由估值而非業績貢獻,畢竟疫情對中公教育的線下業務還是影響比較大的。那麼,站在當前時點,如何看待中公教育?

01

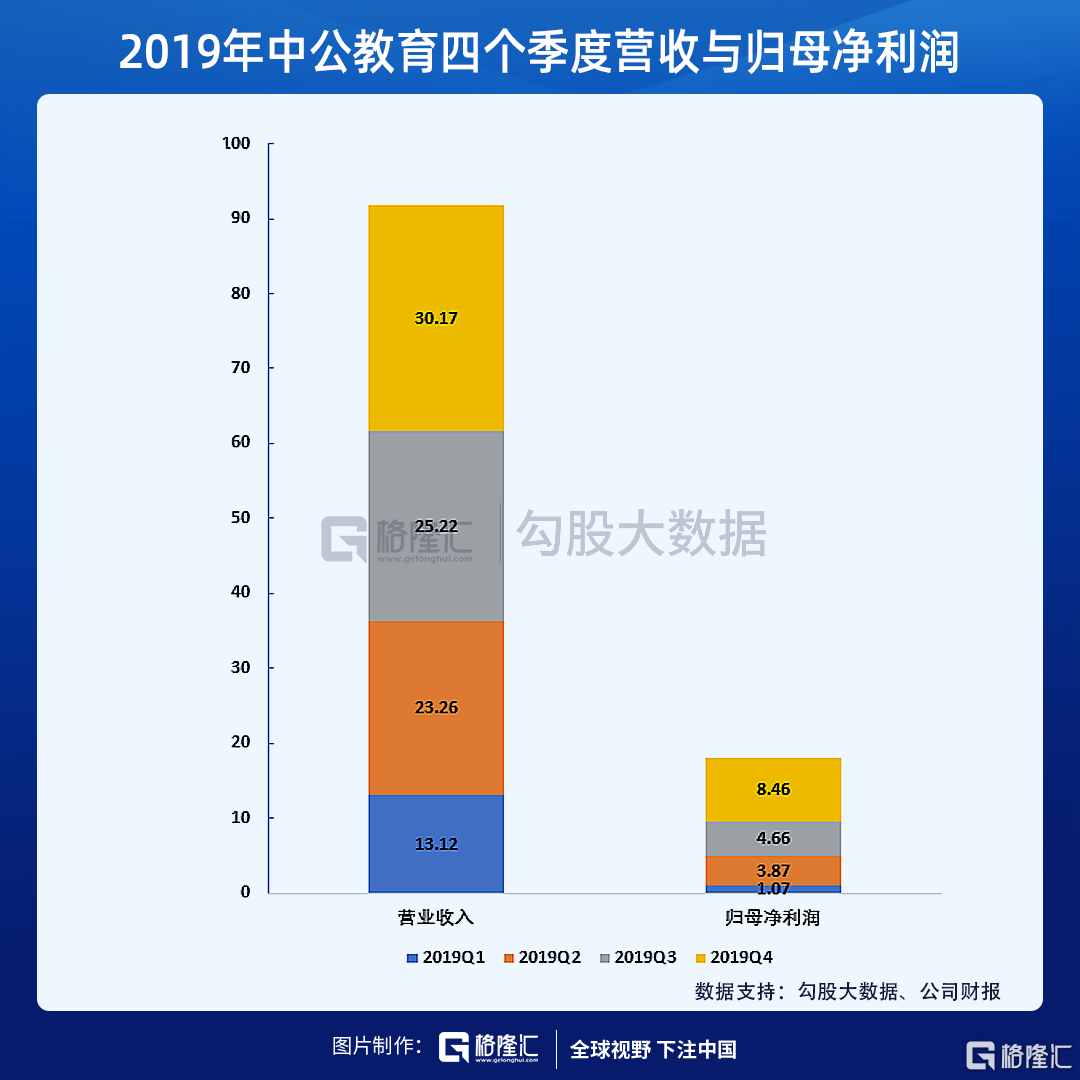

首先是疫情的影響。從財報中看,2020Q1營收同比下降了6.2%,歸母淨利潤則略增8.4%。根據公司前不久發佈的半年報預告,上半年預計淨虧損2~3億元,去年同期為4.93億元,可以看到疫情的影響在財報中有所體現。

其實,疫情的影響已經隨着復產復工復學在逐漸消退,而財報往往是滯後的。財報的作用是證偽,而往往並不能指導投資,投資還是要向前看的。

實際上,疫情對中公教育的影響已經壓縮到了非常小的範圍。主要有三個原因,其一是疫情導致考試(省考、考研複試等)延後,培訓需求自然後延,所以需求並沒有被消滅,而是從一二季度挪到了三四季度;

其二是中公教育的線上平台--中公網校和19直播,在疫情中替代了線下培訓,大量的教學轉到了線上,一定程度上彌補了線下的空缺;

其三則是中公教育一二季度是傳統淡季,以2019年為例,當年上半年營收佔全年營收不到四成,而歸母淨利潤則佔比不到三成。再加上大量的需求被延遲到第三四季度,可以預料,今年剩下的時間,中公教育的業績會是好上加好。

02

回顧中公教育的發展軌跡,2010年以前,其立足於公考,逐漸發展成為全國最大的公務員考試培訓機構。

作為最早的一批公務員考試培訓機構,中公教育在公考領域積累了大量的經驗。2010年後,中公教育逐漸將業務擴張至事業單位、教師培訓、考研培訓等其他品類。

職業考試培訓這個市場,是個大而零散的市場。職業培訓的市場總規模超過千億,完全容得下千億市值的公司,且這個市場還在快速發展當中。職業培訓市場又是由若干個細分市場所組成的,其中比較大的有IT培訓、財會培訓、考研、國考省考培訓、教師資格證考試培訓等等,中小型的有法考、消防工程師考試、MBA等等,種類非常之多。

跨職業、跨學科的巨大差異和地域分佈使得職業考試培訓市場有以下特徵,一個是市場集中度,多以中小機構為主,另一個是全國性龍頭屈指可數。

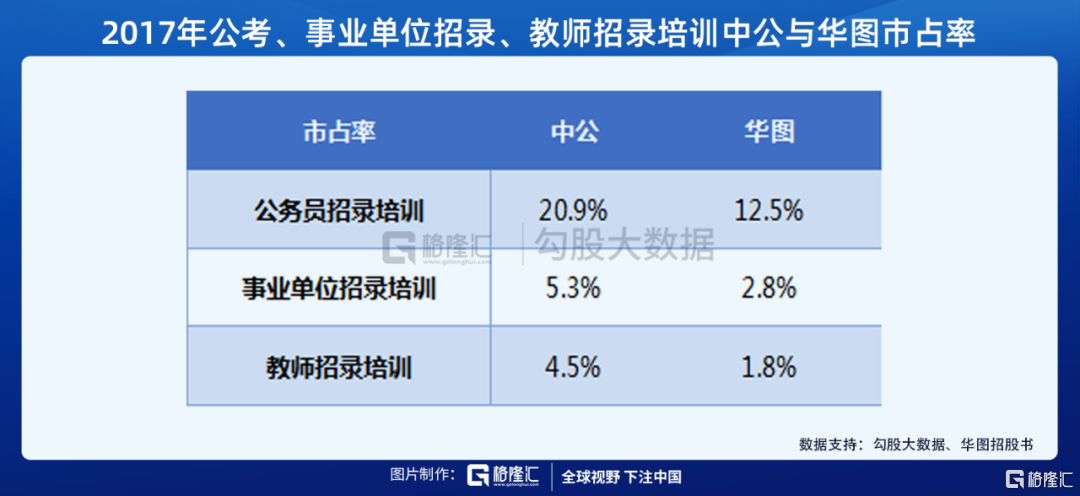

在公考領域,中公教育和華圖教育是市場的No.1和No.2,集中度也已經比較高了。中公教育進入其它細分領域後,憑藉研發優勢+直營渠道優勢+集團化優勢等,完全可以在其他市場複製公考培訓的成功模式。

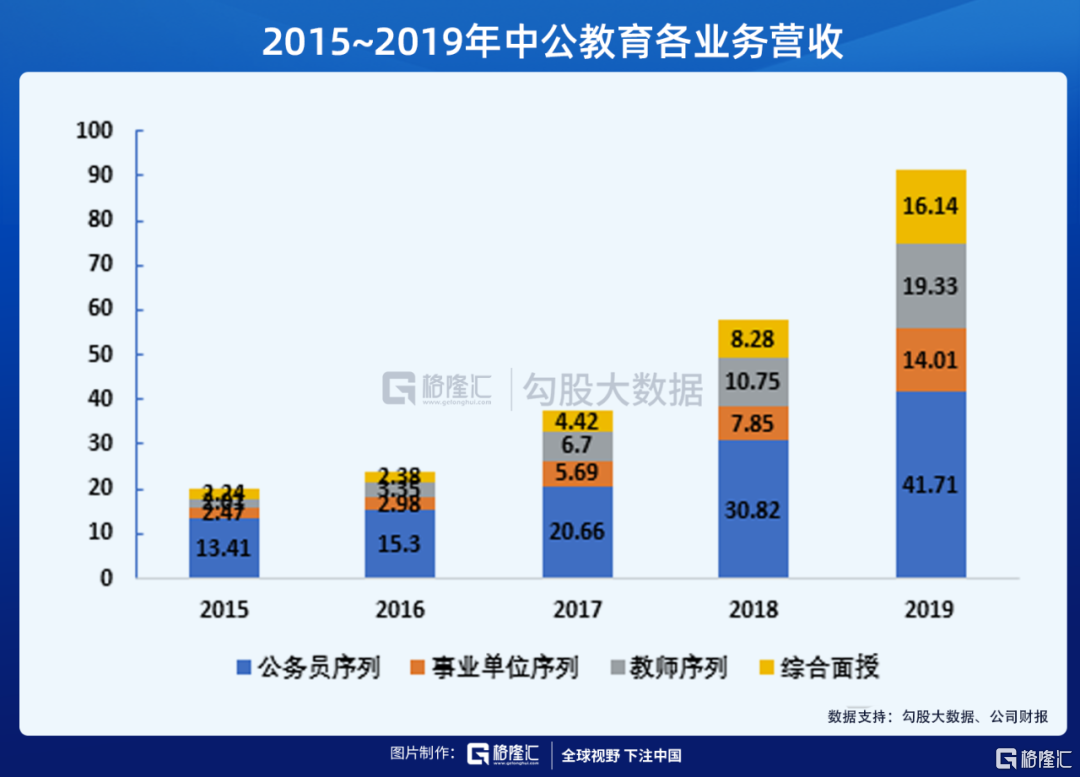

近幾年,中公教育除了立足於公考,其公務員序列培訓收入維持了較快增長,還在其他考試類型,如事業單位、教學資格、考研等考試培訓不斷擴品類。其公務員序列的營收佔比已經從2015年的64.6%下降至去年的45.5%。

配合擴品類,中公教育的直營網點數快速增加,特別是2019年,新增網點數達403個。

中公教育的擴張正好趕上了職業教育的大發展。首先是國家的支持政策密集出台,如去年的《職業技能提升行動方案(2019-2021年)》,提出了2019~2020年開展各類補貼性職業技能培訓5000萬人次以上;其次是職業考試均處於擴容週期,例如今年國考招錄人數大幅增長43%。

正在進行的省考,據統計招錄人數也大幅增加。此外,教師資格考試、研究生考試等報名人數也出現了較大幅度增長。今年可謂是招錄大年,並且在可預計的將來,這一趨勢仍將延續。

03

尾聲

好賽道、好公司、好價格,這三個"好"往往不可兼得。好公司往往不便宜,再加上當下里抱團之風日盛,以至於50倍的茅台,80倍的海天味業,90倍的芒果超媒,乃至於100倍的中公教育,還在不斷的提高估值的上限。合理嗎?沒什麼不合理的,短期看股市就是個投票機,這麼高的估值只不過是資金用腳投票的結果罷了。而長期來看能不能維持住,我們還得掂量掂量"好"的成色。

More Content