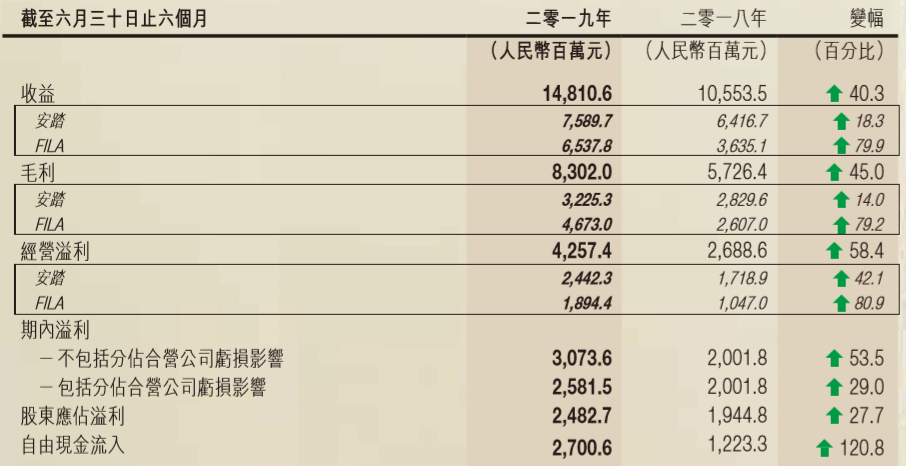

今日午间,近期饱受沽空机构压力的安踏体育(02020.HK)发布上半年业绩报告。报告显示,2019年上半年该公司收益为148.11亿元(人民币,下同),同比增长40.3%;毛利为83.02亿元,同比增长45%;股东应占溢利为24.83亿元,同比增长27.7%。每股基本盈利为92.5分,拟派中期股息每股31港仙。

不过,或是受市场情绪拖累,该公司股价并没有因为中期业绩利好而上涨,反而是低开,但其股价今年以来已累计上涨逾5成。截至今日收盘,其股价报收61.25港元,微跌1.37%,成交额5.4亿港元,最新总市值1654.51亿港元。

业绩再创新高

值得注意的是,该公司的FILA(斐乐)品牌相关财务数据此前遭到沽空机构质疑,但其一直拒绝披露除门店数量外FILA的任何数据,此番是其首次披露FILA的核心数据。

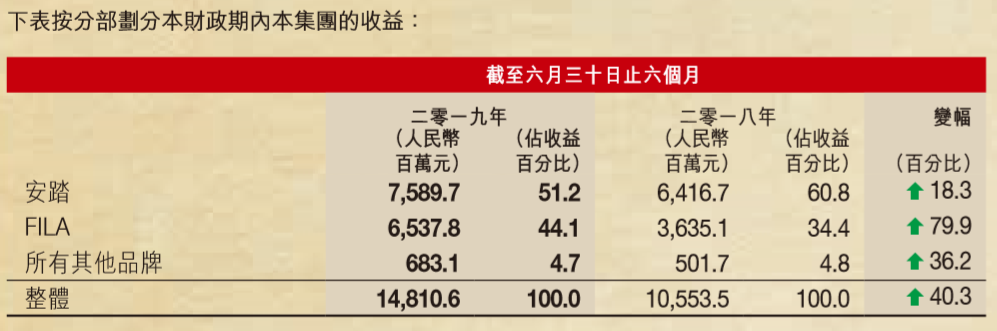

报告显示,今年上半年,FILA收入由36.351亿元增至65.378亿元,增幅79.9%,但较安踏品牌的75.897亿元少逾10亿元,安踏品牌中期收入较2018年的64.167亿元增长18.3%。

期内,FILA实现营业收入65.38亿元,同比增长79.9%,占总营收的44.1%,在中国大陆、香港、澳门和新加坡的门店共1788家,2018年末为1652家。

期内,FILA实现营业收入65.38亿元,同比增长79.9%,占总营收的44.1%,在中国大陆、香港、澳门和新加坡的门店共1788家,2018年末为1652家。

并且,今年上半年,该公司的整体毛利率与2018年同期相比上升1.8个百分点至56.1%。而整体毛利率的上升,主要由于FILA分部贡献增加,而其毛利率相对较高。

该公司表示,今年上半年安踏分部毛利率减少,主要归因于该公司致力于安踏品牌的极致性价比,特别是在鞋类产品上提升产品科技和创新;及策略性给予分销商更多返利,以激励分销商升级安踏品牌九代店,优化分销网络布局及推行零售层面数码化。

不过,该公司的收益主要来自核心分部安踏,其占整体收益的51.2%,而FILA分部贡献了该公司整体收益的44.1%。

报告期内,该公司收益增40.3%至148.1亿元,增幅位居全行业首位;经营溢利增58.4%至42.6亿元;股东应占溢利为24.8亿元,增长27.7%,且连续六年每年均保持近20%的增长;整体毛利率上升1.8个百分点至56.1%;经营溢利率上升3.2个百分点至28.7%;经营现金流入净额达到34.4亿元。

报告期内,该公司收益增40.3%至148.1亿元,增幅位居全行业首位;经营溢利增58.4%至42.6亿元;股东应占溢利为24.8亿元,增长27.7%,且连续六年每年均保持近20%的增长;整体毛利率上升1.8个百分点至56.1%;经营溢利率上升3.2个百分点至28.7%;经营现金流入净额达到34.4亿元。

在FILA与安踏两大品牌的助力之下,该公司今年上半年确实交出了一份亮眼的业绩。

遭浑水五度做空

今年7月初,安踏体育被做空机构浑水Muddy Waters Research做空,称其财务指标造假,令其股价从55.6港元跳水至52.85港元,大跌逾7%,市值蒸发超百亿。

其后,浑水更是一连发布5篇做空报告。至于报告内容,业内人士大体总结为:安踏私底下控制经销商,转移成本;转移实控企业到自己控制的网络手上,套现金额;伪造FILA门店数量及财务数据。

另据报道,浑水在沽空报告里提到,投资者不能相信安踏旗下FILA商店的数量,其称“安踏一直在向其审计人员和公众报告FILA数量,同时声称拥有所有FILA商店。安踏是否从其不拥有的FILA商店合并财务数据?正如我们对安踏品牌财务的看法一样,安踏很可能只是编造了这些数字——也就是说,安踏很可能在FILA品牌方面也报告了欺诈性的财务状况。”

合计起来,在过去的一年多里,安踏体育已经遭受三大沽空机构“光顾”。该公司在去年6月遭受机构GMT Research Limited的做空,而在今年5月底,还遭受机构“杀人鲸”Blue Orca Capital 的做空。

大体上,三家机构的做空报告均指向安踏体育的利润率过高和财务指标真实性。不过从股价方面衡量,该公司股价今年以来已累计上涨逾5成,三家机构的沽空似乎并没有奏效。

大行维持对其评级

不过,由于今年上半年安踏体育的收入及毛利率均胜预期,摩根士丹利今日发表报告称,维持对其「增持」投资评级及目标价67港元。

大摩表示,安踏体育今年上半年销售收入148亿人民币按年升40%、毛利率上升1.8个百分点至56.1%,营运溢利(撇除其他收入)按年升52%,公司同时首次公布安踏自家品牌及FILA品牌分别的销售及盈利数据,相信市场会对此感到正面。

而在7月底,当时安踏体育发布半年报预喜,美银美林发表报告重申对该股的“买入”评级。

美银美林彼时指,目前安踏体育对应2019年及2020年预测市盈率为22倍,低于国际运动用品同业约30倍的水平,因此相信现价尚未反映该公司多个利好因素,其中包括近期业务强劲增长势头及新收购等。该行维持对中国体育用品行业以及安踏未来数年业务前景正面的看法,并相信公司下半年收入增长持续巩固。

More Content