美东时间8月21日周三美股盘前,拼多多(PDD.O)发布了2019年第二季度财报。由于当季营收和每股亏损大幅好于市场预期,股价盘前大增11.71%。从7月15日以来,不包括盘前的涨幅,拼多多的累积涨幅已经达到35% 。

(来源:Yahoo Finance)

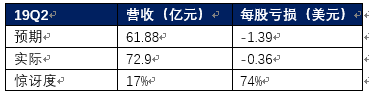

市场预期:

核心数据:

1、 营收:72.9亿元人民币,市场预期61.88亿元,去年同期27.09亿元。

2、 调整后每ADS亏损0.36元,去年同期亏损1.4元,市场预期亏损1.39元

3、 年化活跃买家数4.832亿,同比增长41%,活跃买家的平均年消费额为1467.5元人民币,同比增长92%。

一、核心点评

拼多多依靠拼团+社交的模式快速成长起来,成为如今增长最快的电商平台。这个季度最大的亮点有两个:营收增速没有下滑的迹象,仍然保持野蛮的增长势头; 销售费用率大幅下降,从而令亏损大幅收缩。

之前投资者都担心拼多多在不补贴的情况下就很难维持营收的高速增长。但这个季度的优异表现证明了拼多多在补贴速度放缓的情况下仍然能实现营收的高速增长,打消了投资者的担忧。

二、营收增长的逻辑

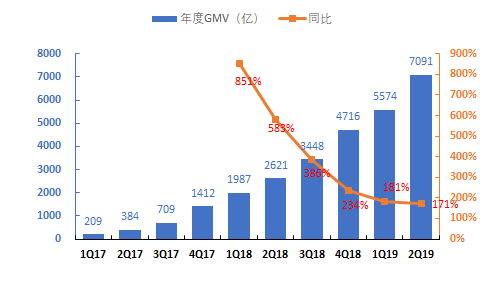

拼多多的商业模式类似于阿里巴巴,属于平台型,所以收入主要来源于广告费和平台佣金。GMV越高,拼多多能从中获取的佣金越高。二季度拼多多年化GMV达到7091亿元,同比增长171%,仍然保持野蛮增长。

CEO黄峥在电话会议上提到,拼多多一、二线城市用户GMV占比上半年提升11%至48%。

拼多多2018年的take rate为2.8%,阿里巴巴剔除新零售,本地服务等业务后,核心电商的take rate为4.37%,拼多多货币化率仍有上涨空间。

(数据来源:拼多多财报)

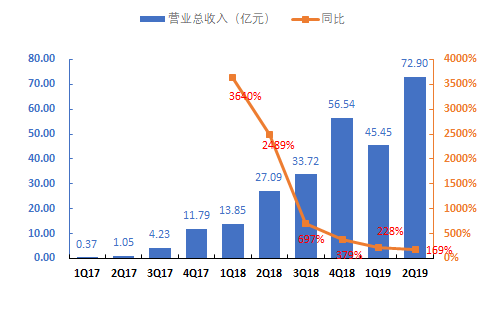

二季度拼多多营收72.9亿元人民币,同比增长169%。其中在线营销服务收入64.7亿元,同比增长173%,佣金收入8.23亿元,同比增长143%。营收的增长主要得益于GMV的增长。GMV得增长则是由更多的活跃消费者和更高的单用户消费额所带动。

(数据来源:拼多多财报)

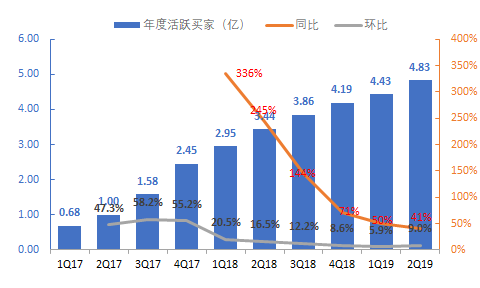

拼多多二季度年度活跃买家达到4.83亿,同比增长41%,环比增长9%。环比净增接近4000万。活跃买家的增长主要得益于618购物节。同时,平均月活跃用户(MAUs)达到3.66亿,同比大增88%,环比增长26%。

(数据来源:拼多多财报)

对比一下二季度三家电商的活跃消费者数,阿里6.73亿,环比增长3.06%;京东3.21亿,环比增长3.3%,拼多多4.83亿,同比增长9.03%。拼多多活跃消费者数已经远超京东,落后于阿里,但环比增速是最快的。

活跃买家的平均年消费额为1467.5元人民币,同比增长92%。人均消费额的增加与拼多多不断扩充平台上的商品品类有关。

三、盈利能力分析

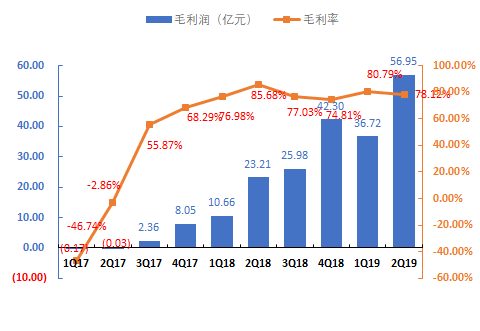

作为平台型电商,一开始就决定了拼多多的毛利率不会低。二季度拼多多实现毛利56.95亿元,毛利率为78.12%,同比下降6.88pct,环比下降2.67pct。二季度营业成本同比上升388%至15.94亿元,主要是因为更高的云服务、客服中心和商户支持服务的成本。

(数据来源:拼多多财报)

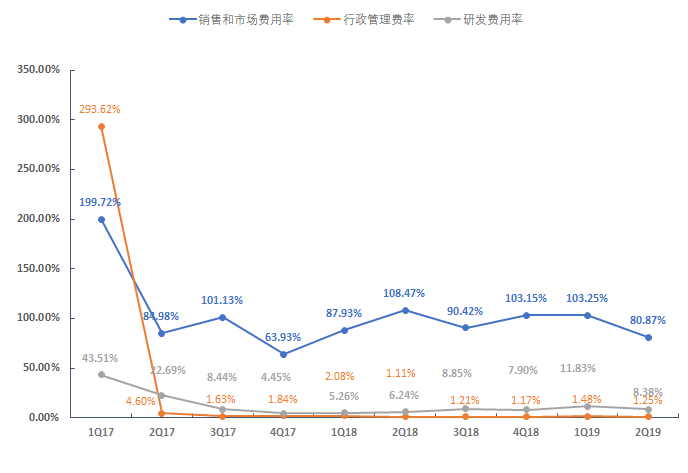

拼多多这个季度第二大亮点就是更好的费用控制,主要体现在销售与市场费用的控制上。二季度Non-GAAP销售与市场费用同比增长101%到58.95亿元,但远远低于营收的增速。可以看出拼多多补贴的力度在放缓,但是并没有影响到消费者的在拼多多平台上的消费力度。

二季度Non-GAAP销售和市场费用率为80.87%,同比大幅下降27.6pct,环比同样下降22.38pct。Non-GAAP行政管理费用率和研发费用率分别为1.25%和8.38%,比较稳定。

(数据来源:拼多多财报)

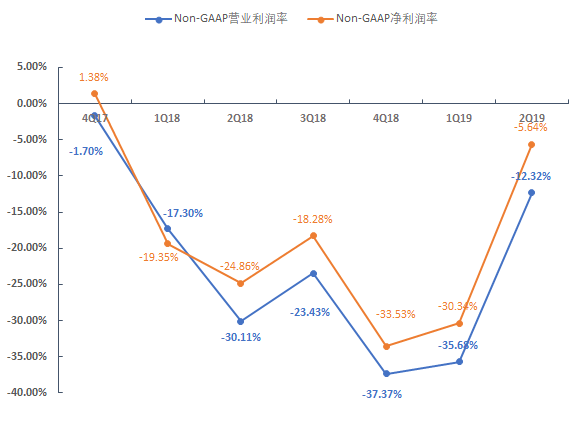

虽然毛利率有所下降,但得益于销售费用率的大幅下降。拼多多净亏损大幅收窄,二季度净亏损10.03亿元人民币,去年同期亏损64.9亿元,Non-GAAP净亏损4.11亿元,上年同期为6.73亿元。

二季度Non-GAAP净亏损率为5.64%,上年同期亏损率为23.86%。如果拼多多下个季度的销售费用率进一步下降,公司将有望盈利。

(数据来源:拼多多财报)

四、结语:

由于拼多多暂时还不盈利,我们尝试使用基于活跃消费者的估值方式对拼多多进行估值。截至8月21日的市值和2019年Q2的年度活跃消费者数进行计算,阿里每活跃消费者估值为705美元,京东单个消费者估值为142美元,拼多多单个消费者估值为100美元。鉴于拼多多仍然处于快速增长期,用户不断渗透到一二线大城市,单用户消费金额提高,同时用平台上的商品品种不断扩展。拼多多单个消费者估值有望进一步提高。

More Content