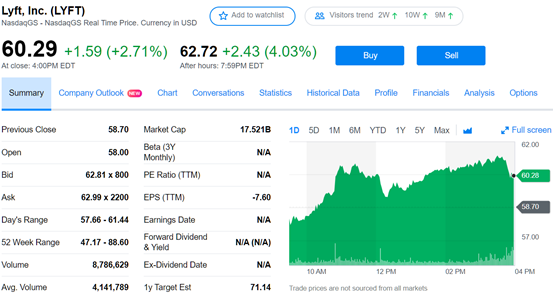

美东时间8月7日周三,网约车第一股Lyft(LYFT.O)发布了2019年第二季度财报。由于当季营收好于市场预期,每股亏损有所收窄, 盘后股价一度上涨13%,但之后公司宣布禁售股将提前在8月解禁, 股价回吐了一些上涨。

(来源:Yahoo Finance)

市场预期:

Lyft Q2财报亮点:

1、 营收:8.67亿美元,同比增长72%,市场预期为8.09亿美元;

2、净亏损: 6.44亿美元,去年同期亏损1.79亿美元;

3、 调整后净亏损1.97亿美元,上年同期净亏损1.76亿美元。调整后每股亏损0.68美元,市场预期每股亏损1.58美元;

4、 调整后EBITDA亏损为2.04亿美元, 上年同期亏损1.9亿美元。

一、核心点评

今年3月,顶着网约车第一股光环的Lyft在Nasdaq挂牌上市,IPO定价为72美元。共享经济鼻祖之一的Uber也在之后上市,同样跌破发行价。与今年上市的SaaS企业的股价表现相比,Lyft和Uber的表现可以称得上是难兄难弟。市场对“共享经济“的冷淡,主要是因为他们仍然看不见共享经济商业模式下的盈利方式。

与Uber的全球化战略不同,Lyft只专注于北美市场,全球化路径尚不明确。在业务发展战略上,Uber更加多元化,而Lyft主要专注于共享出行的业务,包括共享单车及滑板车租赁,Lyft还与众多无人驾驶出租车商进行合作,同时公司也在大力发展To B业务从而促进增长。 Lyft目前的看点是如何控制成本,从而扭亏转盈。

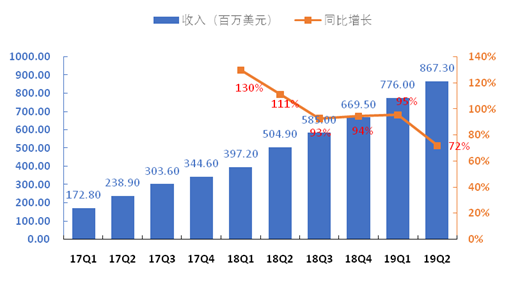

二、营收分析

Lyft在19年第二季度营收为8.67亿美元,同比增长72%,高于分析师预期8.09亿。公司将高速的增长归功于市场需求的增长。同时,活跃乘客数量和每位活跃乘客支出的增加推动收入增长。可以说是“量价”双提升。

(数据来源:Lyft财报)

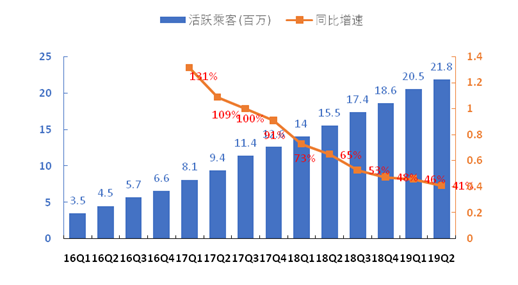

截至19年Q2,活跃乘客达到创记录的 2180万,同比增长41%。公司认为大部分新增用户都是有机增长的,公司并没有通过大量的市场营销来进行获客。上半年公司围绕IPO的宣传也对获取新的乘客产生了积极的作用。

(数据来源:Lyft财报)

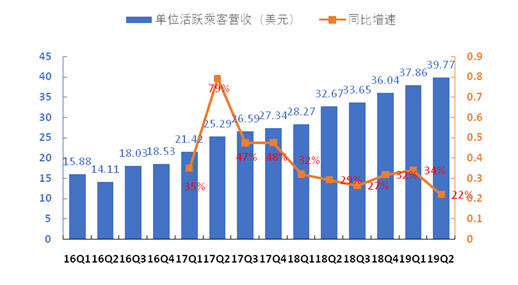

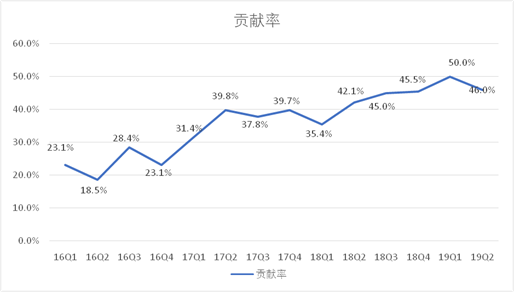

Q2单位活跃乘客营收39.77美元,同比增长22%。通过电话会议的信息可知,公司在6月底进行了提价,但提价的影响暂时没有体现在Q2了。公司预计提价的影响将提高每单位活跃乘客营收增加1%。

(数据来源:Lyft财报)

三、盈利能力分析

营收的增长并不是现阶段投资者关注的点。投资者最关心的是网约车模式究竟能否盈利。网约车的商业模式有点像电商平台。其中电商平台的GMV相当于网约车平台的订单总金额,平台从订单中抽取佣金,所以营收关键点在于平台的Take Rate。

从Take rate中我们可以看到网约车对司机的补贴程度,补贴越高,take rate越低,平台能赚取的利润就越低。

遗憾的是,但Lyft并没有在季度财报中公布订单总金额或者Take Rate的数据,所以我们无法知道平台的货币化率。2018年Q4的take rate为28.7%。其实Take rate的提升空间有限,就像直播平台一样,每做一笔生意,就要给司机分成,分成比例是固定的,也不存在规模效应。

第二个就是看Contribution Margin(相当于平台毛利率)。Lyft平台的毛利率是相当高的,第二季度Contribution Margin达到46%,同比上涨3.9个百分点,环比下降4%。Contribution Margin同比上升是因为公司对费用的控制能力提高,环比下降是因为投资了共享单车及滑板车租赁设施。预计2019年毛利率的提升不大。

(数据来源:Lyft财报)

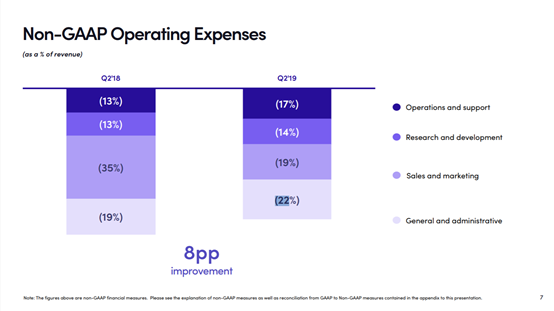

第三个从费用端下手。Non-GAAP情况下,公司第二季度运营与支持,研发,销售与营销和行政费用分别占营收17%,14%,19%和22%。其中运营与支持,研发和行政费用占比同比上升,销售和营销费用占比大幅下降。

销售费用主要包括对乘客的推广活动产生的费用。消费费用的大幅下降主要得益于今年IPO对品牌有推广作用。预计未来费用率将得益于营收规模的扩大而下降。

(来源:Lyft2019Q2财报)

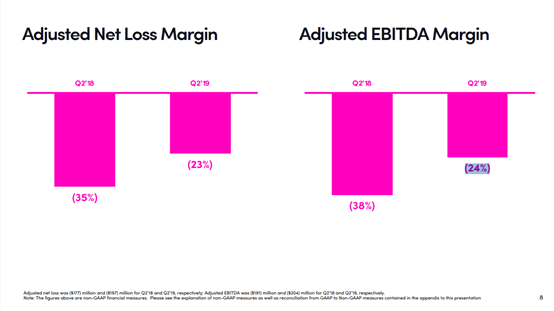

Lyft第二季度净亏为6.44亿美元,包括IPO股权支出和监管保险负债变化支出。调整后净亏损1.97亿美元,调整后净亏损率为23%,

调整后EBITDA亏损为2.04亿美元, 上年同期1.9亿美元。调整后EBITDA亏损率24%。虽然亏损绝对值稍微扩大,但亏损率在缩窄。

(来源:Lyft2019Q2财报)

四、结语:

截至美东时间8月7日,Lyft总市值175.21亿美元,P/S(TTM)=7.05x,Uber总市值673.13亿美元,P/S(TTM)=5.84x。仅从市销率上看,Lyft比Uber还贵一些。

不管是Uber还是Lyft,都没有证明网约车模式如何盈利。从Lyft这个财报来看,关键Take rate没有公布,Contribution Margin暂时没有提高的空间,费用率的下降并不足以能让公司盈利。这也是为什么市场不看好网约车双雄的原因。

很多大行预计Lyft在2022年后EBITDA转正, Lyft和Uber究竟谁能成为第一个盈利的共享经济公司呢?拭目以待明天Uber的Q2财报。

More Content