创梦天地(1119.HK)中国独树一帜的手游发行商首次给予买入评级目标价6.2港元

机构:招商证券

评级:买入

目标价:6.2港元

■ 创梦天地是中国首屈一指的独立手游发行商

■ 游戏收入主要受ARPPU及付费率上升驱动

■ 我们预测2018-21年收入和经调整净利润的复合年增长率分别为21%和30%,我 们首次覆盖创梦天地并给予买入评级;目标价为6.2港元

腾讯力挺的中国多功能游戏平台

创梦天地是中国领先的独立手游发行商,曾发行过多款知名海外休闲游戏,包括: 地铁跑酷、神庙逃亡2、纪念碑谷和梦幻花园等。公司也充当内容提供商的角色, 并自主研发了如魔力宝贝和全民冠军足球这样的高质量游戏。通过基于源代码和本 地化经验的精细化游戏运营,创梦天地能够大幅度延长游戏的生命周期,因此能转 化更多的客户终身价值。其大型的用户基础(平均MAU约1.3亿),也为公司提供 了充足的变现机会。更重要的是,创梦天地和腾讯建立了坚实的战略合作伙伴关 系,并在内容、技术和商业化上都有密切合作。

游戏是现金牛;线下体验店潜力巨大

我们认为游戏业务仍将是公司的现金牛,预期该业务在2019/2020/2021年将实现 29%/19%/17%的同比增长,分别占总收入的90%/90%/89%。收入的快速增长主要 源于:1)ARPPU的快速提升(2019年预测:人民币28.1元;2020年预测:人民 币31.1元;2021年预测:人民币34.7元),和2)付费率的提升(2019年预测: 5.8%;2020年预测:6.0%;2021年预测:6.0%)。这是由于公司更为专注于具 有较高ARPPU和付费率的中重度游戏类别,如RPG、SLG和消除类游戏。除此之 外,创梦天地在娱乐新零售方面的试点 - 好时光影游社,一旦能利用腾讯的资源 找到一个可复制的盈利模式,也具有巨大潜力。

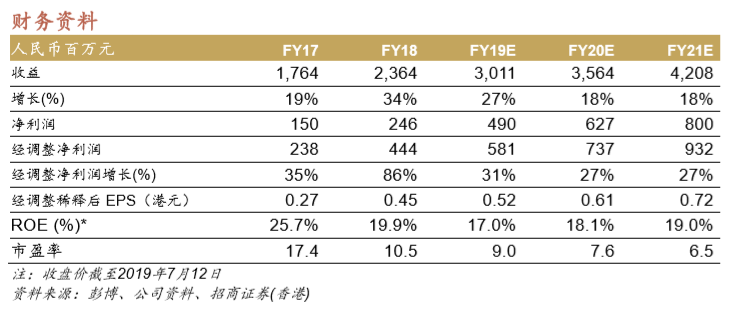

财务预测

我们预测2018-2021年,公司总收入及经调整净利润将分别以21%和30%的复合年 增长率增长。我们预测同期游戏收入将以22%的复合年增长率增长。对于非游戏业 务,我们预期线上广告将以8%的复合年增长率增长,而线下体验店的收入将由 2018年约5百万元人民币增长至2021年的1.19亿元人民币。我们预期毛利率将由 2018年的44%扩张至2019年的46%、2020年的47%及2021年的47%,主要驱动因 素为:1) 魔力宝贝及全民冠军足球以净额法确认收入;2)公司利用自营分发渠道 令渠道成本比率下降,以及3) 自主研发游戏数目增加从而减少内容成本比率。

首次覆盖,给予买入评级;目标价6.2港元

我们相信,作为游戏平台创梦天地的收入更为多样化,因此将不太受手游发布的高 不确定性所影响。另外,我们看好公司能够延长其游戏生命周期的能力,以及它在 腾讯生态系统内特殊且稳固的地位。我们首次覆盖创梦天地,给予公司 6.2 港元的 目标价。我们采用了市盈率估值法,给予创梦天地 79 亿港元的估值(基本情况), 这是基于本地对标公司平均 12.0 倍的 19 年预测市盈率。悲观和乐观情况:我们得 出股价区间为 5.6 港元至 6.9 港元,相当于 10.8 倍至 13.2 倍 2019 年预测市盈 率。

Follow us

Find us on

Facebook,

Twitter ,

Instagram, and

YouTube or frequent updates on all things investing.Have a financial topic you would like to discuss? Head over to the

uSMART Community to share your thoughts and insights about the market! Click the picture below to download and explore uSMART app!

Disclaimers

uSmart Securities Limited (“uSmart”) is based on its internal research and public third party information in preparation of this article. Although uSmart uses its best endeavours to ensure the content of this article is accurate, uSmart does not guarantee the accuracy, timeliness or completeness of the information of this article and is not responsible for any views/opinions/comments in this article. Opinions, forecasts and estimations reflect uSmart’s assessment as of the date of this article and are subject to change. uSmart has no obligation to notify you or anyone of any such changes. You must make independent analysis and judgment on any matters involved in this article. uSmart and any directors, officers, employees or agents of uSmart will not be liable for any loss or damage suffered by any person in reliance on any representation or omission in the content of this article. The content of the article is for reference only and does not constitute any offer, solicitation, recommendation, opinion or guarantee of any securities, virtual assets, financial products or instruments. Regulatory authorities may restrict the trading of virtual asset-related ETFs to only investors who meet specified requirements. Any calculations or images in the article are for illustrative purposes only.

Investment involves risks and the value and income from securities may rise or fall. Past performance is not indicative of future performance. Please carefully consider your personal risk tolerance, and consult independent professional advice if necessary.