來源:宏觀芝道

導讀:

2022年,美國經濟一條容易被忽略的主線是財政補貼對居民資產負債表的改善,以及如何刺激後續需求。

若看不到這一邏輯,我們不僅會忽視上半年美國內需的強度,更會低估下半年美國經濟的韌性。

我們認爲,下半年美國居民消費增速不弱,企業資本支出仍有韌性。隨之而來的,是高燒難退的通脹,和不會輕易轉鬆的貨幣政策。

要點:

市場對於美國經濟衰退的預期已愈演愈烈。我們認爲,美國下半年總需求趨勢下行,然而下行幅度和節奏或不如市場預期的那樣強烈。美國GDP增速爲負,這一經濟衰退現象,今年下半年未必能看到。2022年下半年,我們預計美國衰退也許會遲到。

今年上半年美國經濟動能已經被市場低估

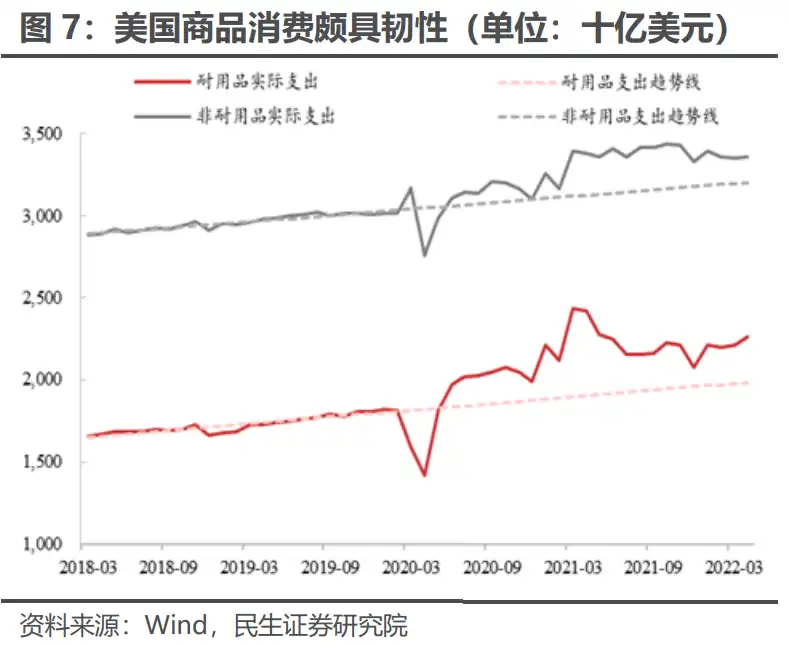

2022年上半年美國經濟最重要的關鍵詞必然是「高通脹」。與高通脹相伴,美聯儲迅速加息和縮表。然而迅速大幅貨幣收緊之下,上半年美國內需體現出驚人韌性。商品消費和企業資本開支超越市場預期。居民超額儲蓄和消費信貸,二者支撐起上半年美國強勁內需。

錯估美國經濟韌性,本質上是忽略了居民資產負債表改善對總需求的拉動

把視角從2022年抽出,我們會發現本輪經濟週期實因疫情後歷史級別的財政刺激而起。假如說,2021年美國經濟的主題是財政補貼對居民當期收入的改善,那麼2022年我們便需要關注財政補貼對居民資產負債表的改善如何刺激後續需求。

今年下半年美國需求韌性同樣不可低估。

首先,下半年美國居民消費不會弱。

首先,下半年美國居民消費不會弱。

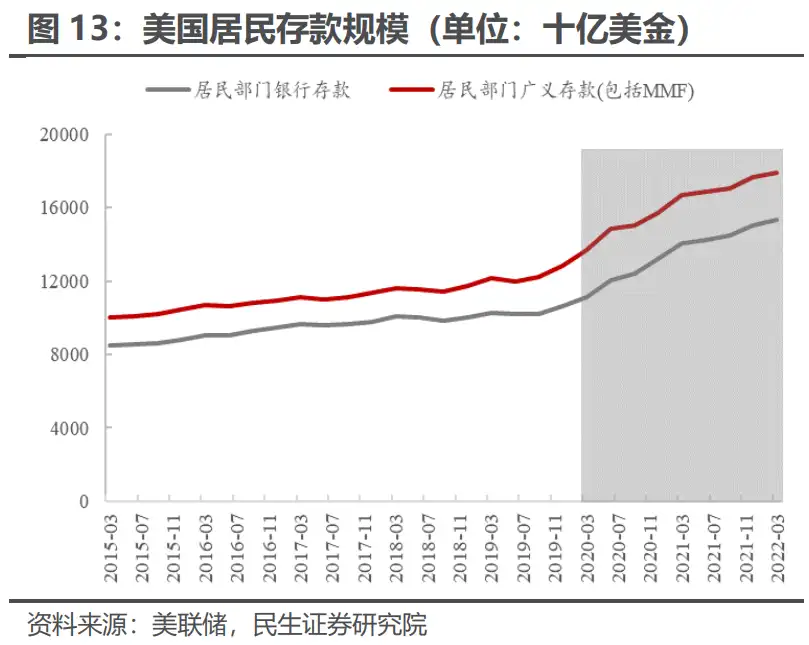

未來較高的工資增速將帶動美國居民消費。同時,強勁的收入和超額儲蓄仍將支撐美國居民的財務狀況,從而支持消費信貸增長。「工資+儲蓄+信貸」,美國居民廣義收入仍然健康,消費也會有韌性。

其次,企業資本開支增速或許會邊際下行,但仍有韌性。

企業是否進行資本開支通常受兩個因素決定:終端需求和融資成本。居民消費已經決定終端需求不弱,但未來美聯儲快速的加息會擡升企業的融資利率。

下半年美國經濟風險主要在地產

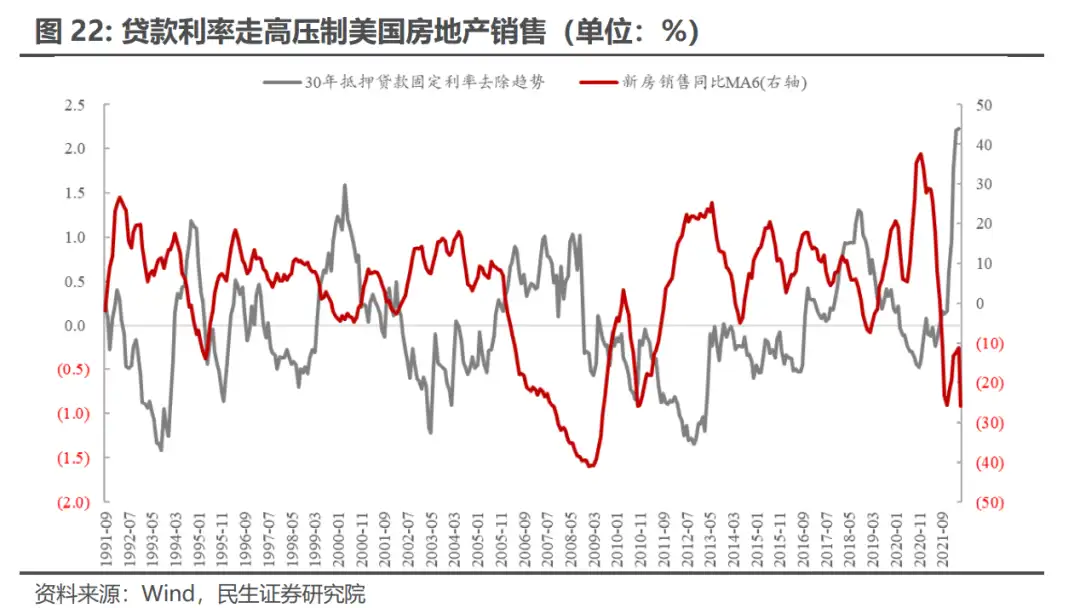

當然,下半年美國經濟並非沒有風險點,最大的逆風項來自房地產鏈條。

在高利率下,房地產銷售勢必受到壓制。我們預計下半年美國房地產銷售將繼續放緩,從而拖累房地產投資和相關地產消費。我們認爲本輪地產下行不會帶來房價的大幅下跌,加上當前美國居民資產負債表相對健康。從概率上判斷,我們預計下半年美國地產崩盤可能性低。

通脹難「退燒」,貨幣收緊趨勢難言拐點

通脹方面,因地緣政治及產能有限等原因,大宗商品價格仍處於易漲難跌狀態。疊加未來美國較高的工資增速和租金通脹,我們預計美國通脹年內高燒難退。

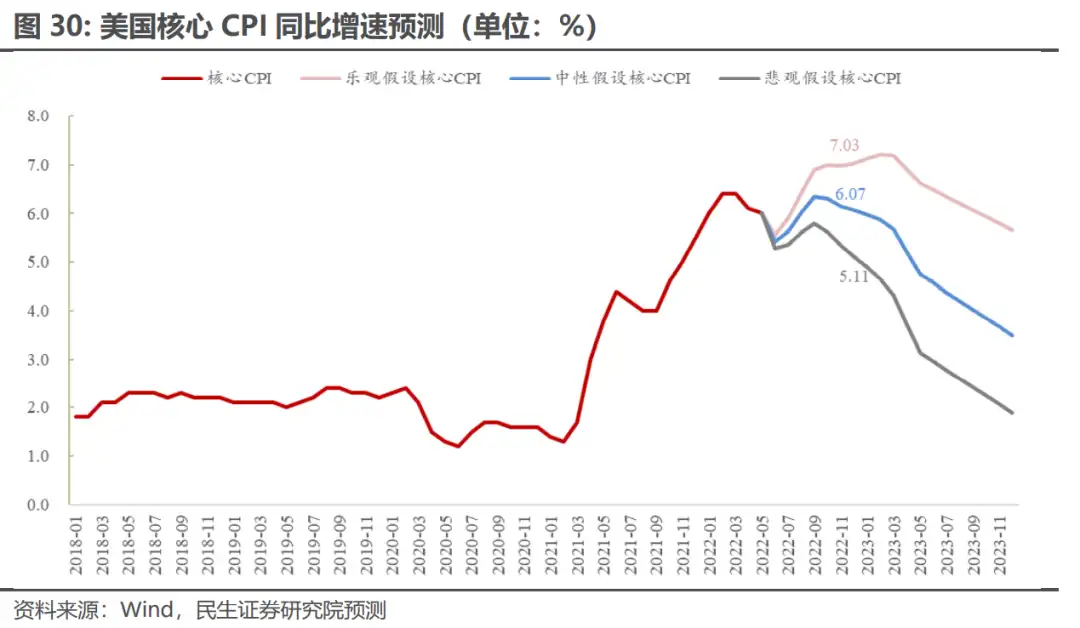

經測算,2022年末,美國CPI同比增速仍在7.9%的高位,核心CPI同比爲6.1%,遠高於美聯儲目標區間。

要討論美聯儲的貨幣政策,首先需要明確的是,馴服通脹是美聯儲目前的核心訴求,美聯儲政策僅錨定通脹。

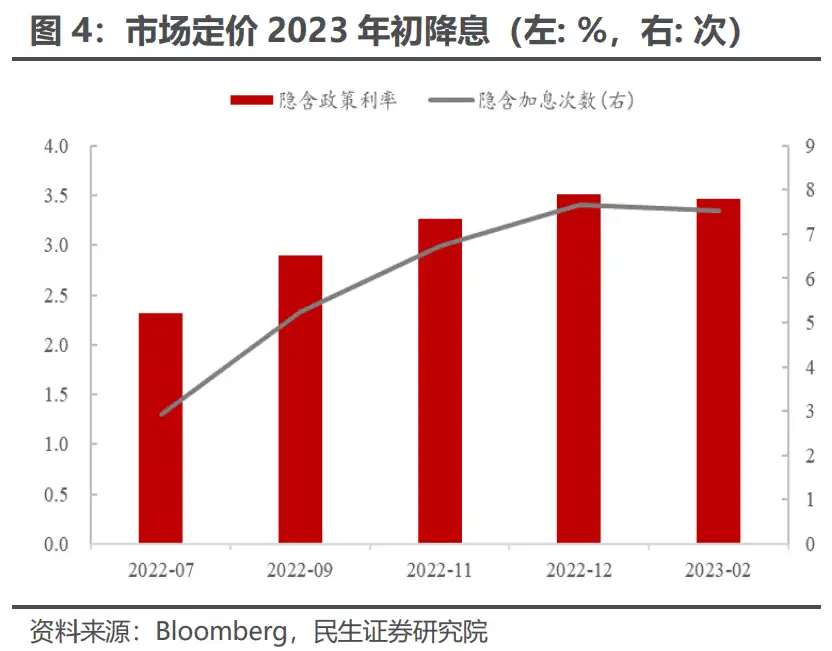

在如此高企的通脹增速下,美聯儲將繼續實行快速加息戰略,

我們預計在下半年的四次會議中,基準加息路徑或爲「75-50-50-25(BP)」。

在貨幣政策快速收緊和實體經濟韌性仍存的環境下,美債利率或未見頂。

當前美債利率下行主要受市場「衰退恐慌」的情緒影響。若下半年實體經濟的韌性得到兌現,對通脹和貨幣緊縮的擔憂將重新主導市場,屆時美債利率或將繼續上行。另外,本輪美聯儲縮表或對銀行體系準備金衝擊較大,不能忽視其流動性影響。

More Content