本文來自格隆匯專欄:中金研究,作者:林英奇、許鴻明等

5月15日,人民銀行和銀保監會發布《關於調整差別化住房信貸政策有關問題的通知》,將首套房個人住房貸款利率下限調整為LPR減20bps(此前為LPR),二套房個人住房貸款利率下限不變(LPR加60bps)。

評論

Q1:為何此時下調?

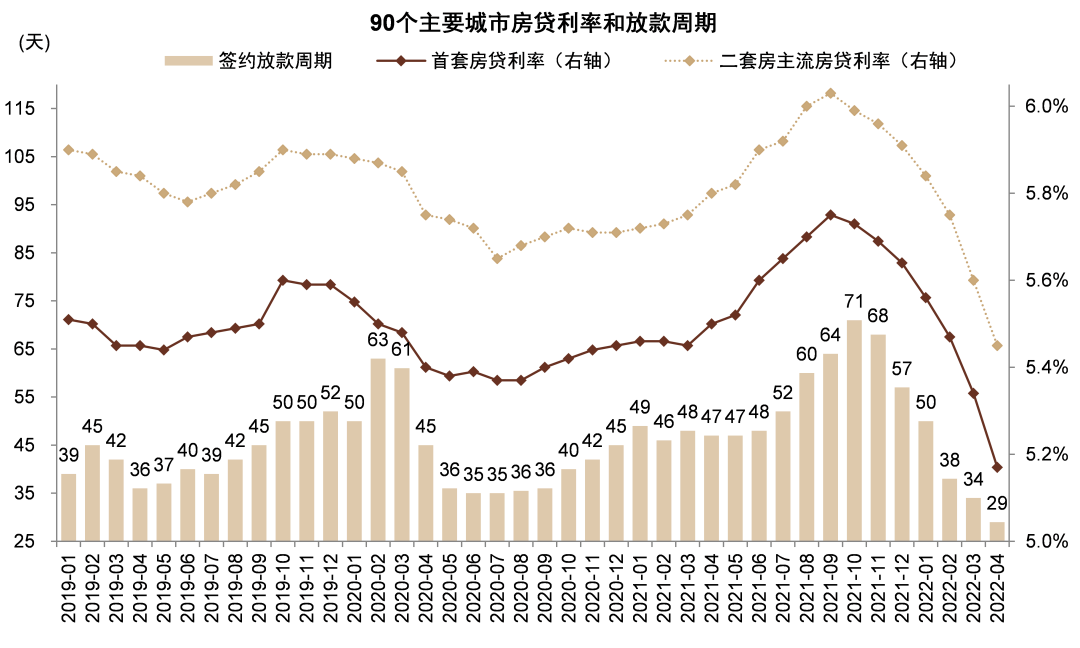

本次按揭利率下限下調是2021年10月以來房地產貸款放鬆的延續,2022年4月主要城市平均新發放住房按揭貸款利率約為5.2%,2021年10月以來已下調約60bps,部分城市已接近5年LPR 4.6%的下限,我們認為利率下限下調旨在為進一步下調實際按揭利率打開空間。從歷史上來看,當前平均按揭利率5.2%仍高於LPR約60bps,相比基準利率的溢價位於歷史較高水平,假設降至4.4%的理論下限則有80bps的下調空間。考慮到購房需求仍較弱,我們預計未來一至兩個季度按揭利率可能繼續下行,每月下調幅度約為10-20bps。

Q2:利率下調對按揭貸款需求的影響?

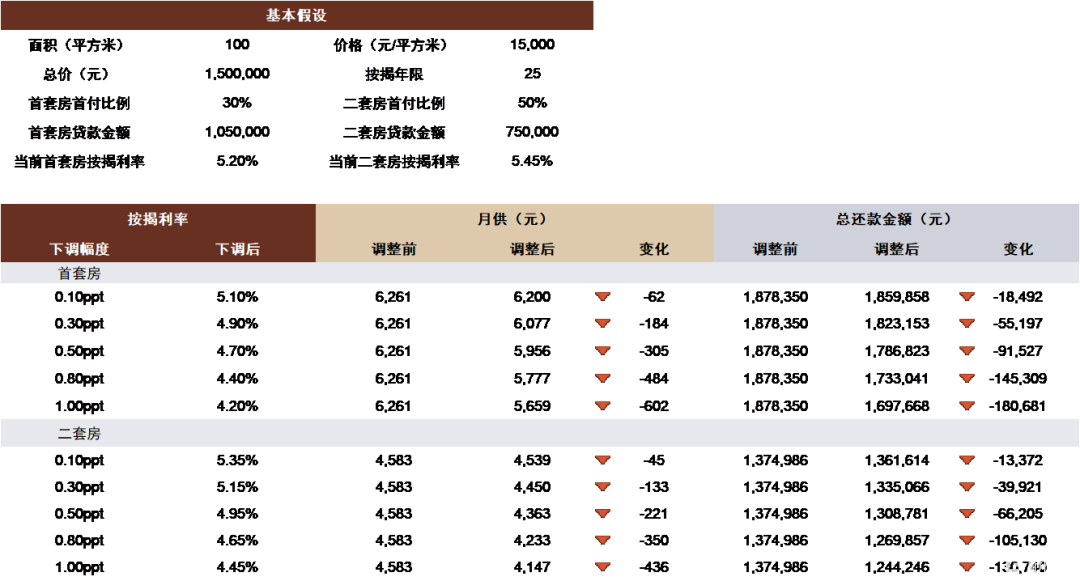

從微觀角度,按揭利率下調能夠降低購房者利息負擔從而刺激貸款需求。假設住房總價150萬元、30%首付比例、25年等額本息還款,按揭利率下降80bps降低購房者月供約500元,降低總還款額14.5萬元。除利率外,住房升值空間和首付比例同樣是借款者考慮的主要因素,同樣假設下我們測算年回報率提高1ppt能夠提升5年後價值約10萬元,首付比例下調10ppt能夠降低購房門檻15萬元。從歷史經驗來看,過去三輪按揭貸款降息週期中,住房銷售和按揭貸款增速能夠回升10-60ppt,除降息外還包括首付比例和購房門檻下調等配套政策以及房價預期回升的影響,與當前不完全可比。考慮當前住房購房需求仍偏弱,我們預計今年按揭貸款增速下滑幅度能夠企穩在7.5%左右,後續仍需繼續觀察其他政策和購房需求的變化。

Q3:對銀行息差和利潤的影響?

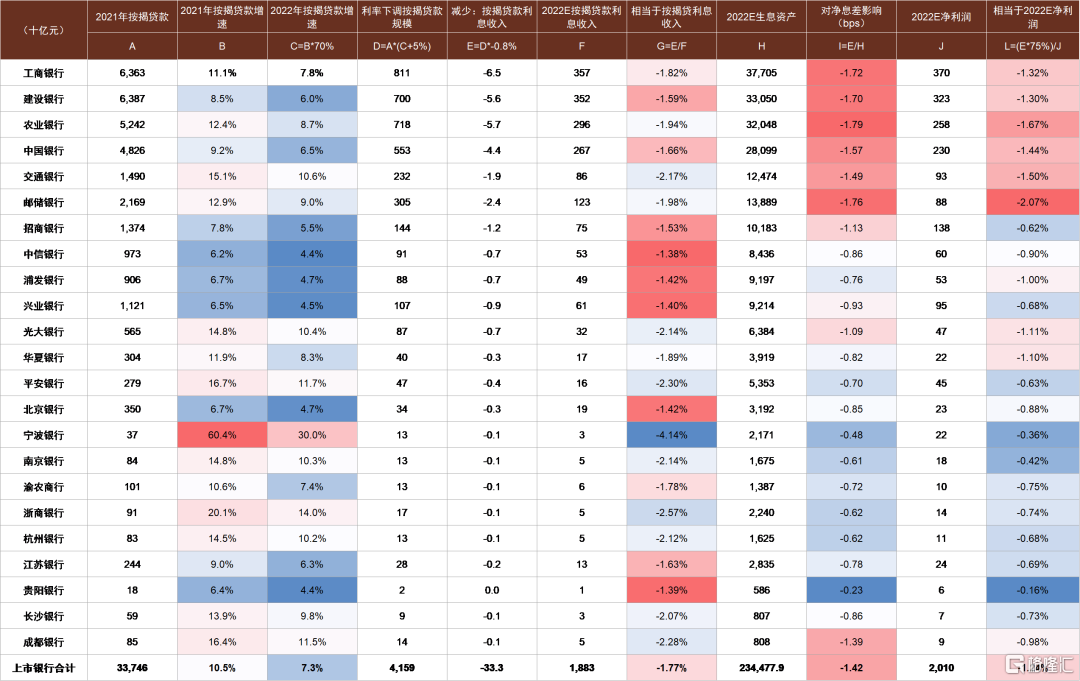

由於利率僅影響新發放貸款,不影響存量貸款定價,因此對銀行收入直接影響較小。假設新發放按揭貸款利率下調80個基點,我們測算每年降低銀行按揭貸款利息/淨利潤/淨息差約1.8%/1.2%/1.4bps。綜合考慮其他因素,我們認為房地產放鬆政策對銀行影響正面,主要由於1)利率下調刺激銷售,銀行可“以量補價”,按揭貸款增速提升2ppt即可抵消利率下調影響; 2)房地產市場放鬆政策能夠降低按揭和開發貸敞口資產質量風險。

風險

按揭貸款增速下滑超預期,違約風險超預期上升。

圖表1:2021年10月以來房貸利率和放款週期已降至2019年以來最低水平附近

資料來源:萬得資訊,中金公司研究部

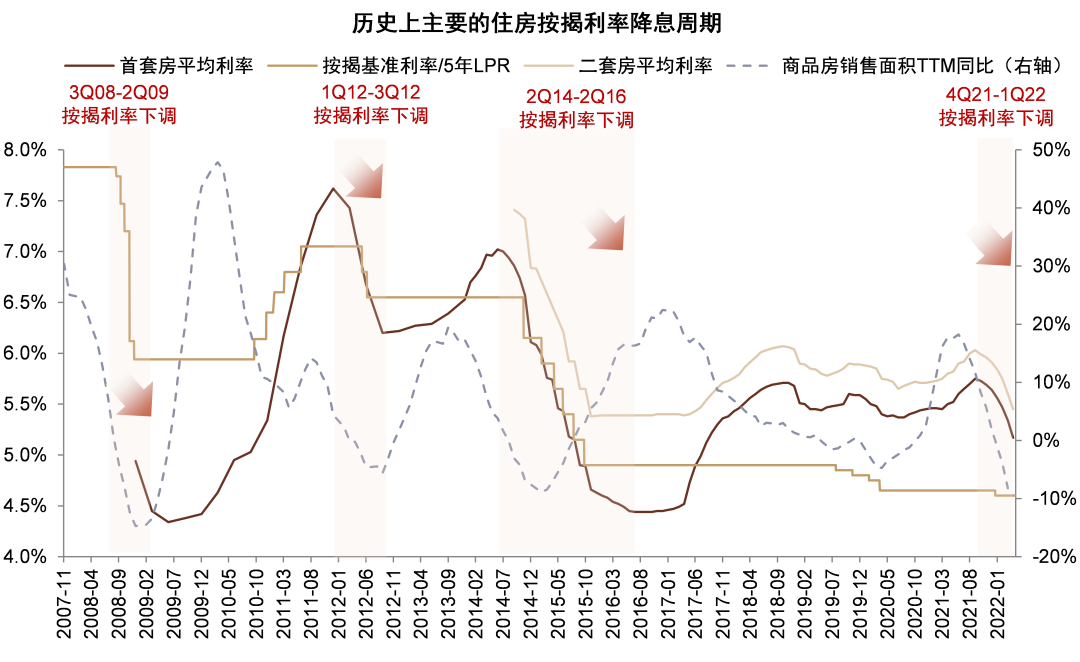

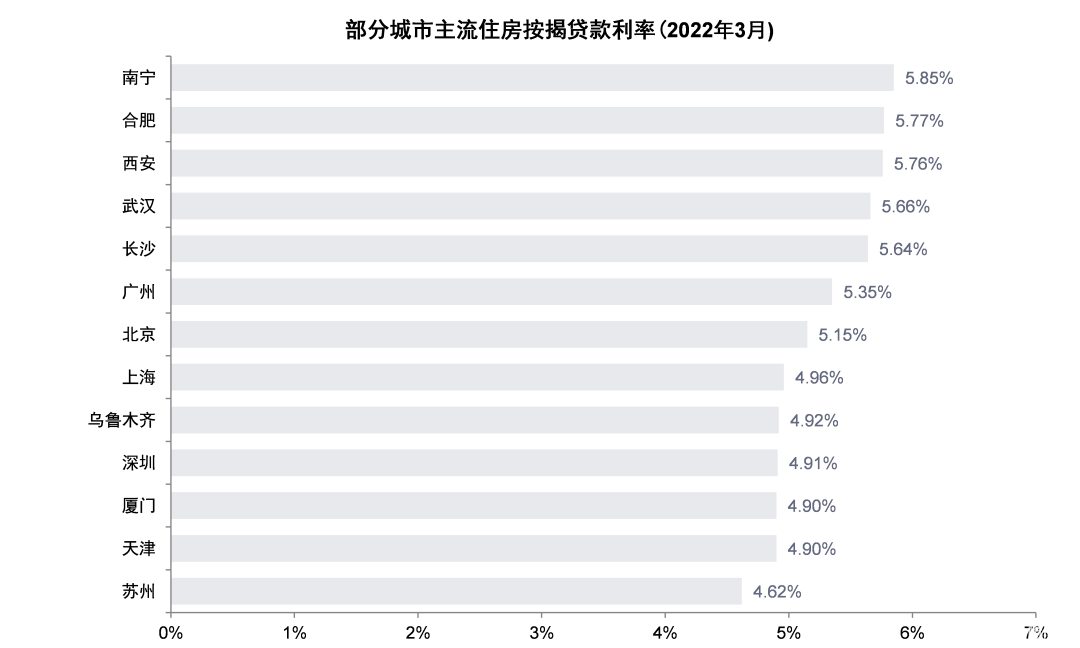

圖表2:2022年4月首套房按揭利率約5.2%,仍高於基準利率約60個基點

資料來源:貝殼研究院,萬得資訊,中金公司研究部

圖表3:我們測算新發放按揭貸款利率下調80bps每年降低銀行按揭貸款利息/淨利潤/淨息差約1.8%/1.2%/1.4bps

注:1) 假設2022年銀行按揭貸款增速為2021年的70%;2)假設每年銀行償還按揭貸款規模為5%;2)假設銀行按揭貸款收益率下降80個基點

資料來源:萬得資訊,中金公司研究部

圖表4:我們測算按揭貸款利率下調80bps降低購房者月供約500元,降低總還款額14.5萬元

資料來源:萬得資訊,中金公司研究部

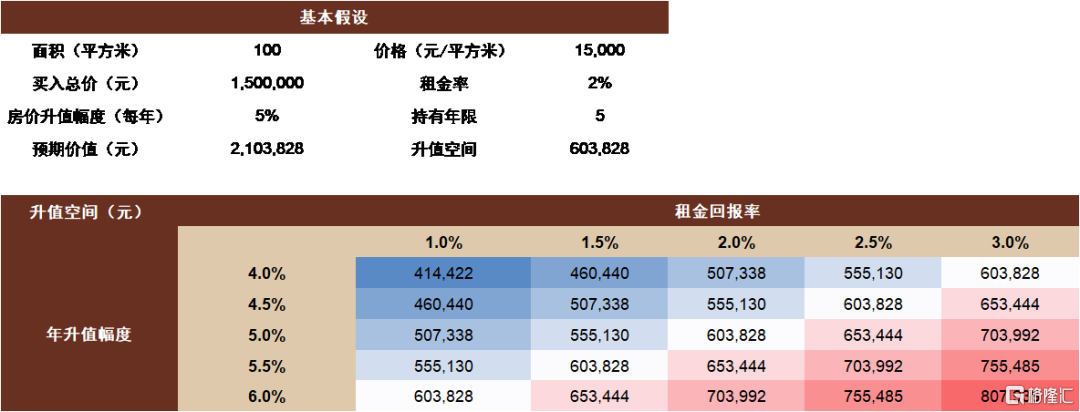

圖表5:我們測算住房價值升值幅度提高1ppt能夠提高5年後升值空間約10萬元

注:住房預期價值包括租金回報

資料來源:萬得資訊,中金公司研究部

圖表6:我們測算首付比例下調10ppt能夠降低購房門檻約15萬元

資料來源:萬得資訊,中金公司研究部

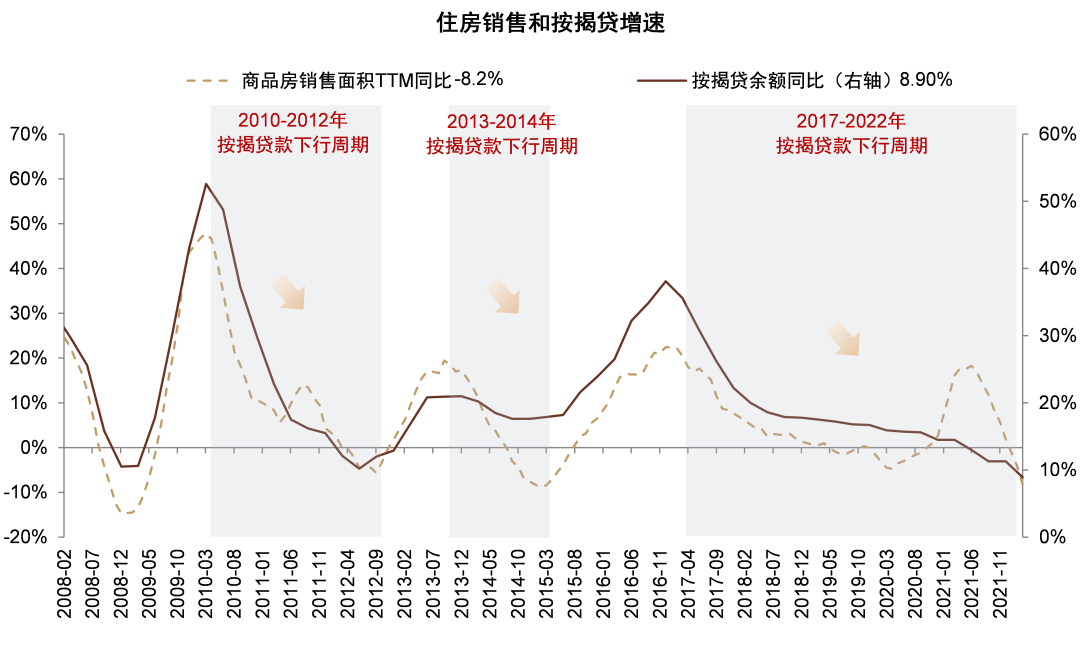

圖表7:2022年1季度按揭貸款增速進一步創歷史新低,降至8.9%

資料來源:萬得資訊,中金公司研究部

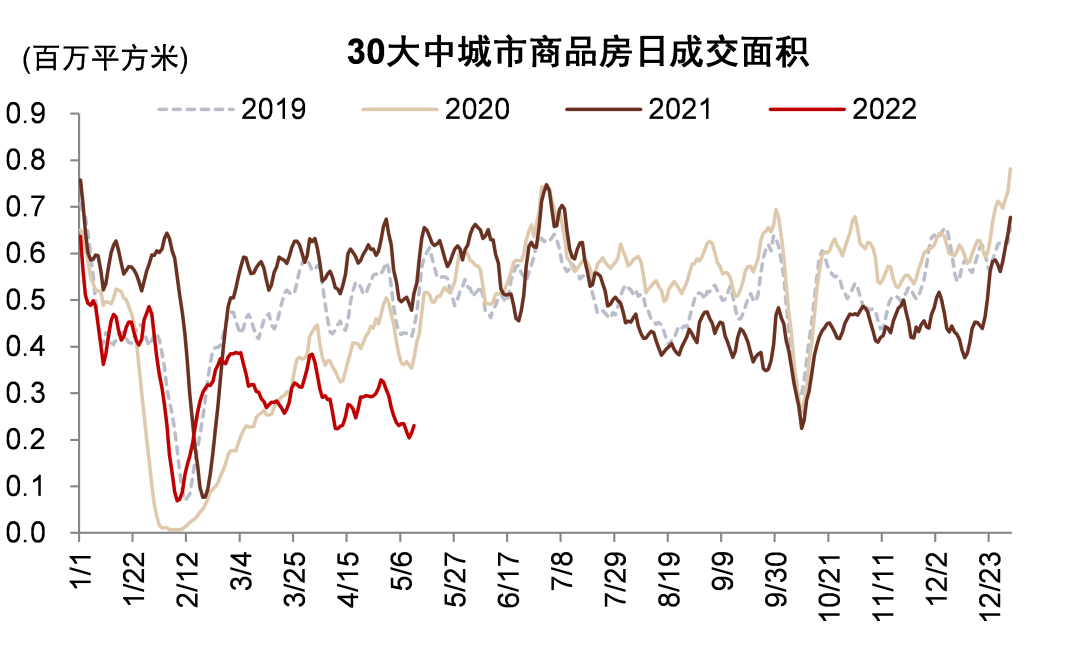

圖表8:2022年4月房地產成交面積明顯下滑,居民購房意願仍然偏弱

資料來源:萬得資訊,中金公司研究部

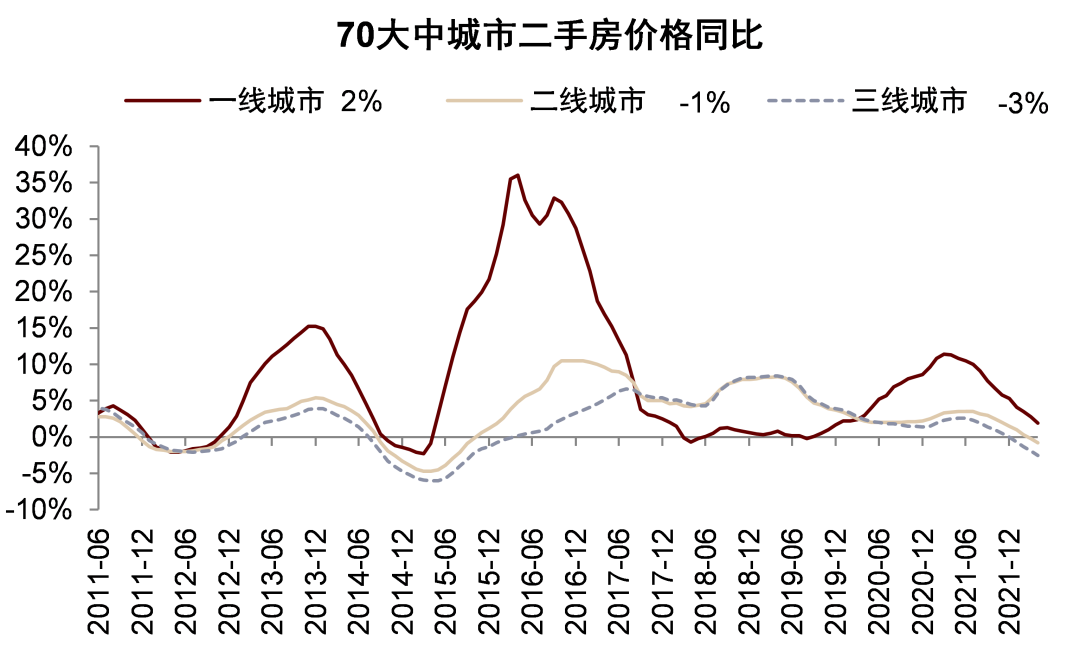

圖表9:2021年下半年以來房價漲幅放緩,二三線城市房價漲幅更加低迷

資料來源:萬得資訊,中金公司研究部

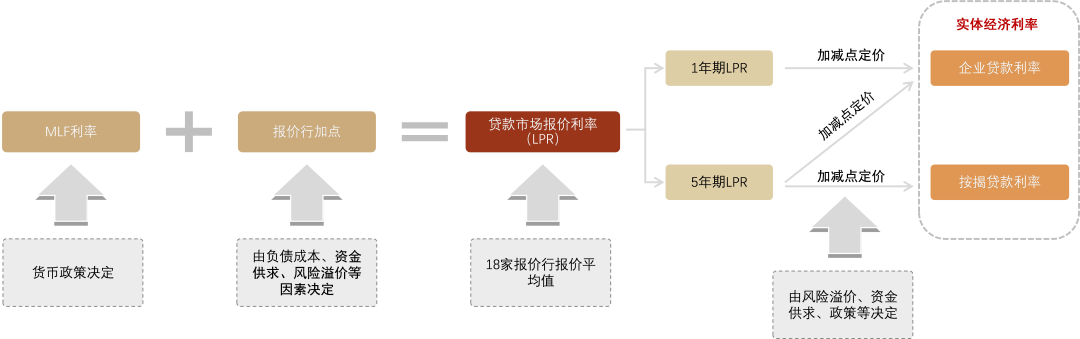

圖表10:個人住房按揭貸款利率由5年LPR加減點形成形成

資料來源:中國人民銀行,中金公司研究部

圖表11:各城市按照“因城施策”的原則制定當地銀行住房按揭貸款利率下限,銀行根據要求設定實際利率

資料來源:萬得資訊,中金公司研究部

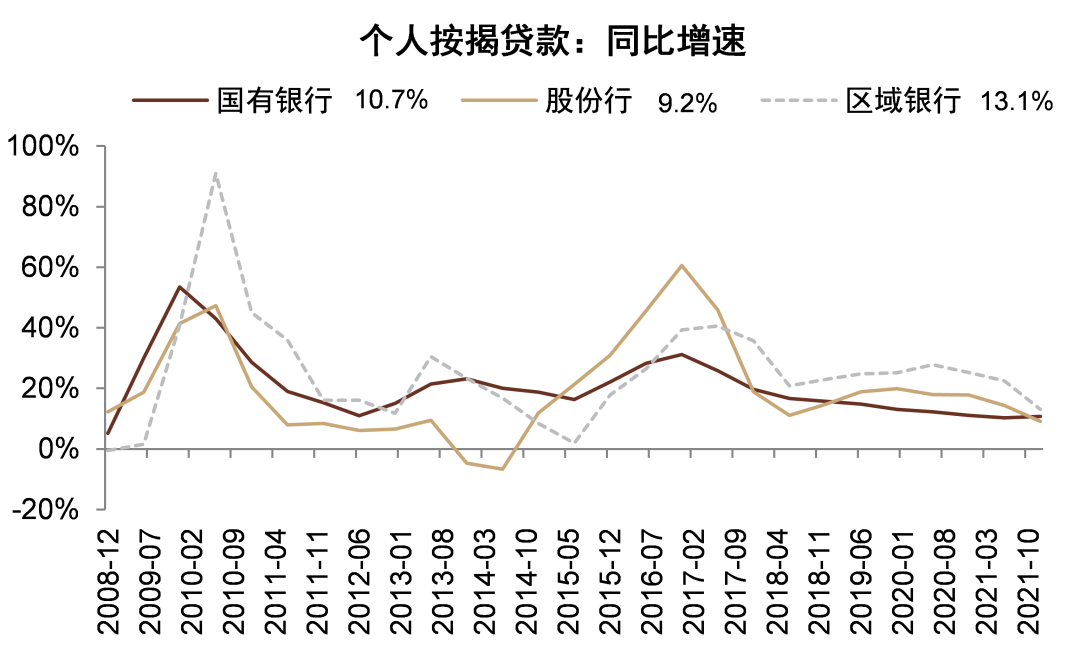

圖表12:2021年中小銀行按揭貸款同比增速下降較多

資料來源:萬得資訊,中金公司研究部

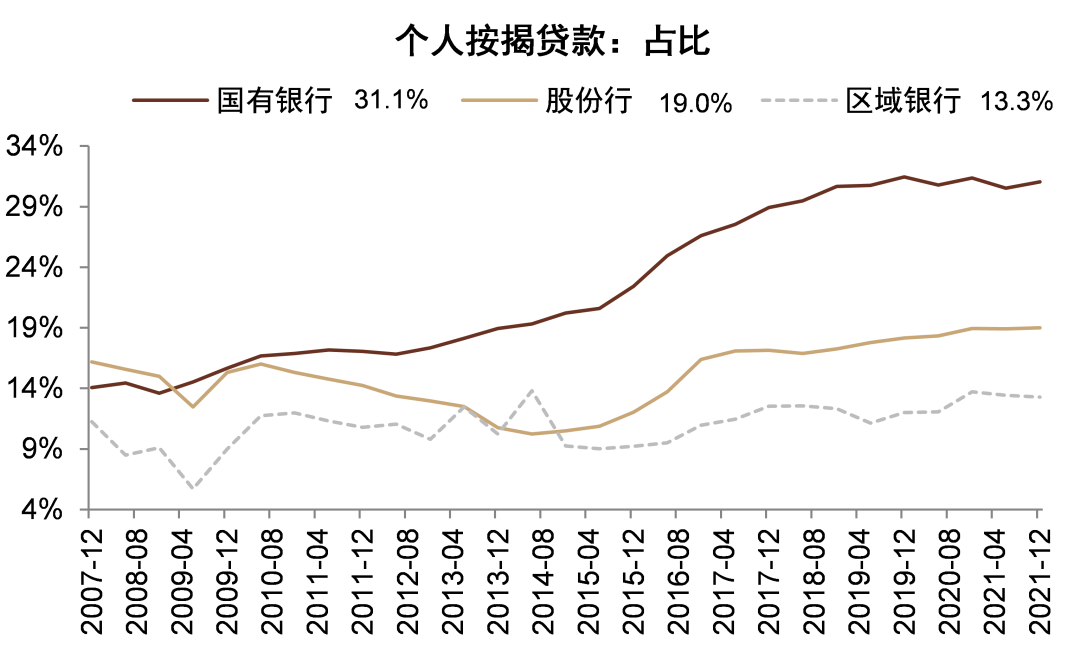

圖表13:銀行按揭貸款佔比基本保持穩定

資料來源:萬得資訊,中金公司研究部

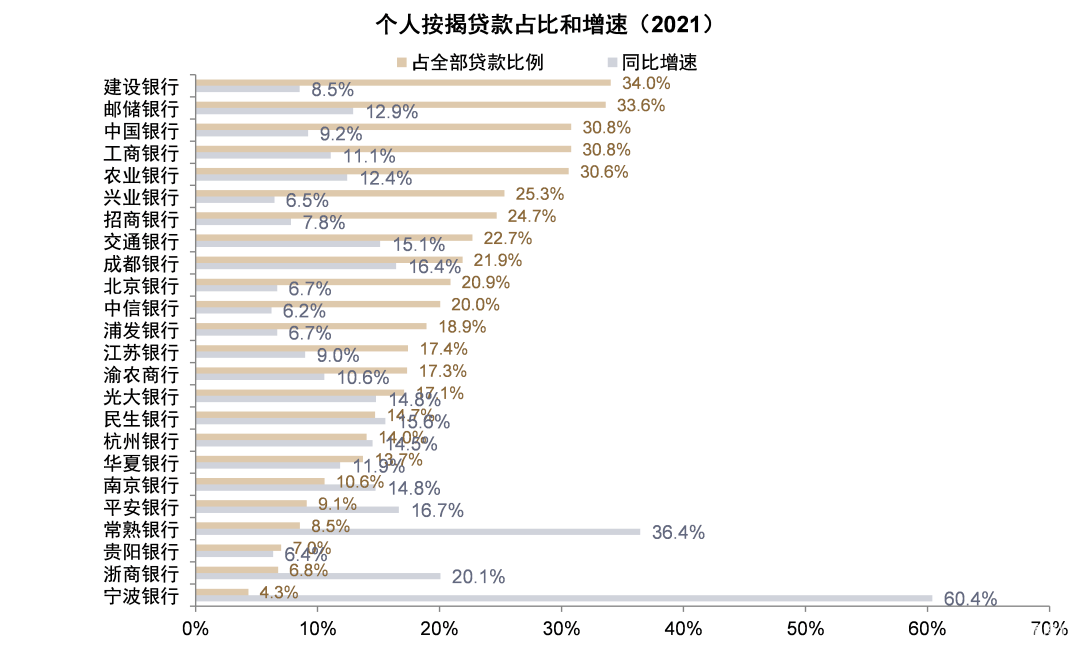

圖表14:國有大行個人按揭貸款佔比較高,部分區域行按揭貸款增速較快

資料來源:萬得資訊,中金公司研究部

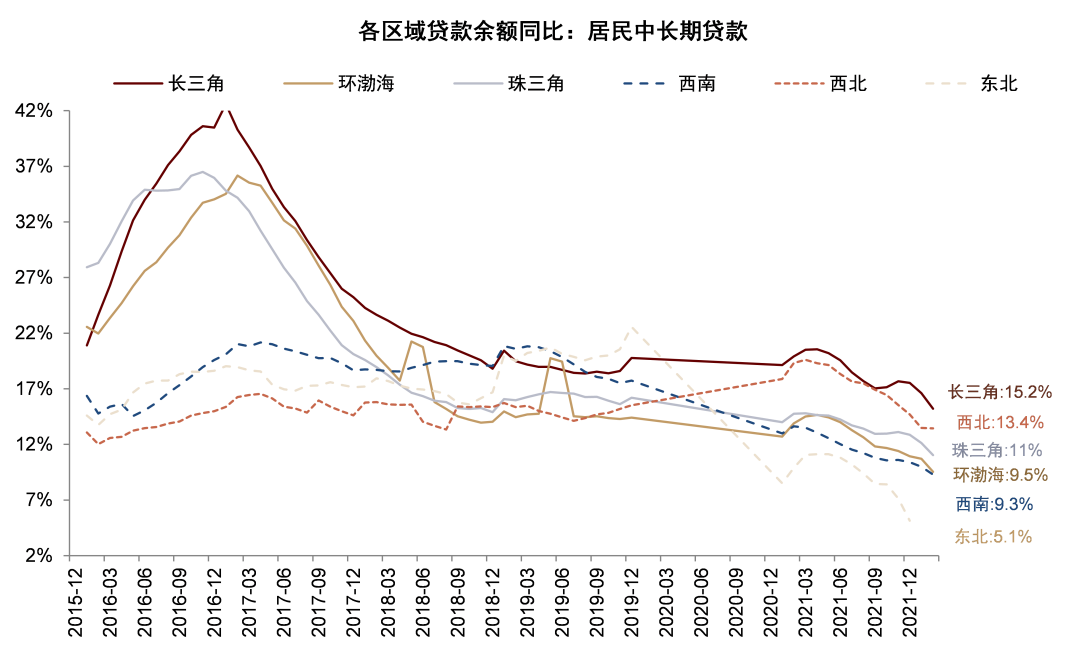

圖表15:2022年3月長三角和西北地區的居民中長期貸款增速較快

資料來源:萬得資訊,中金公司研究部

More Content