據深交所官網消息,北京嘉曼服飾股份有限公司(以下簡稱“嘉曼服飾”)於3月23日首發上會,公司擬在創業板上市,東興證券為其保薦機構。

嘉曼服飾本次擬募資5.21億元,主要用於營銷體系建設項目、電商運營中心建設項目、企業管理信息化項目及補充流動資金。

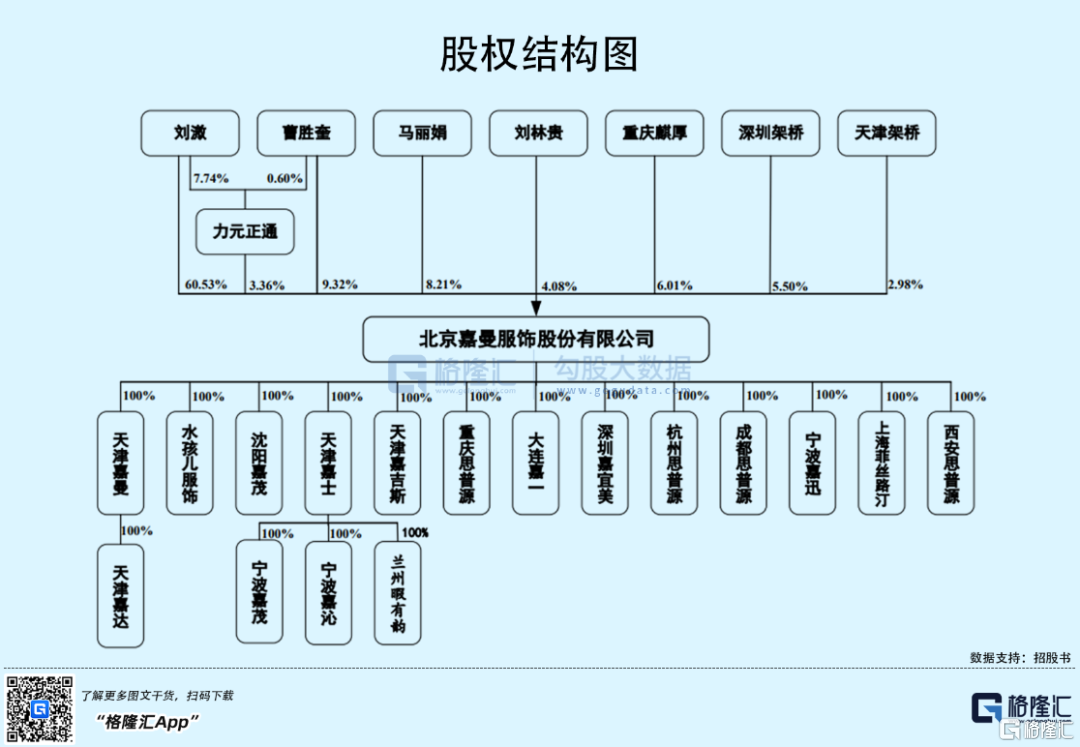

截至發行前,公司的控股股東及實際控制人為曹勝奎、劉溦、劉林貴和馬麗娟,四人合計直接和間接控制公司85.50%的股份。

1

授權品牌毛利率較高

嘉曼服飾是一家中高端童裝運營企業,公司主要產品包括自有品牌水孩兒、授權品牌暇步士和哈吉斯、國際零售代理品牌 EMPORIO ARMANI、HUGO BOSS 等童裝產品。

由於童裝產品的範圍可以覆蓋0-14歲,時間跨度較長,因此童裝市場需求一方面取決於新生嬰兒數量,另一方面主要受兒童人口基數的影響。

2020年末我國0-14歲的人口數量約2.53億人,佔總人口比例為17.95%,我國兒童人口基數較大。但自2017年以來,我國人口出生率呈現下降趨勢,我國新生嬰兒數量從2016年的1846萬人下降至2020年的1203萬人。

儘管如此,近年來,隨着國民人均收入的增加使得消費者的購買力和購買意願都大大增強,消費者願意更多的在孩子身上投入,童裝購買量和價格均持續上漲,以致我國童裝市場零售額從2011年的964億元增長至2020年的2292億元。

我國童裝市場集中度較為分散,根據中國商業聯合會與中華全國商業信息中心出具的《全國大型零售企業暨消費品市場2020年度監測報吿》顯示,在2020年中國大童童裝市場子類別中(國內品牌且不含運動童裝品牌),嘉曼服飾旗下“水孩兒”品牌的市場綜合佔有率僅為0.84%,排名第七。

財務方面,2018年至2021年1-6月報吿期內,嘉曼服飾實現營業收入分別為7.29億元、8.97億元、10.43億元和5.36億元;歸母淨利潤分別為6982.12萬元、8948.38萬元、1.19億元和8788.89萬元,公司的營收和淨利潤均呈現上升趨勢。

據嘉曼服飾未經審計的財務報吿顯示,公司2021年度營收為12.14億元,較上年同期增長16.38%,歸母淨利潤為1.95億元,較上年同期增長63.83%,歸母淨利潤增幅較大。

2020年以來,由於授權經營品牌及國際零售品牌提高銷售價格,導致嘉曼服飾的主營業務毛利率有所提升,報吿期內,公司的主營業務毛利率分別為52.26%、50.65%、50.44%及55.25%。

其中,公司的授權經營品牌及國際零售品牌毛利率高於可比公司平均水平,而自有品牌水孩兒的產品定位下調為中端,產品的吊牌價格隨之下調,導致毛利率水平下降。

另外值得注意的是,嘉曼服飾母公司資產負債率明顯高於合併層面資產負債率,報吿期內,公司合併資產負債率分別為47.6%、44.53%、47.89%和38.17%,而母公司資產負債率要高出近一倍,主要原因是母公司向天津嘉曼、寧波嘉迅採購水孩兒及哈吉斯品牌成衣,形成較大金額的應付款項,導致負債總額明顯高於資產總額。

2

依賴線上銷售渠道

嘉曼服飾的營收規模持續增長,除受益於我國童裝行業持續向好的宏觀因素外,主要得益於公司多品牌運營業務規模的持續擴張以及電子商務業務的快速發展。

截至2021年6月30日,嘉曼服飾在全國31個省、自治區、直轄市開設有659家線下門店,其中直營店鋪199家,加盟店鋪460家;同時在唯品會、天貓、京東等國內知名電商平台開設了37家線上店鋪。

其中,報吿期內,公司線上銷售收入佔主營業務收入的比例分別為 42.75%、52.91%、61.59%和62.17%,而其中通過唯品會、天貓、京東三家電子商務平台銷售收入佔九成左右,存在線上銷售收入佔比較高且集中的風險。同時,嘉曼服飾也是同行業可比上市公司中線上銷售佔比最高的公司。

另外,目前嘉曼服飾持有暇步士童裝和哈吉斯童裝兩個授權品牌,報吿期內,授權經營品牌的營收佔主營業務收入比重分別為51.44%、56.53%、59.42%和 61.49%,佔比較高且有上升趨勢。

雖然嘉曼服飾擁有暇步士童裝和哈吉斯在中國大陸地區(不包括港澳台)的獨家授權,但並不擁有以上兩個品牌在中國境內的商標所有權,未來公司存在一定的品牌授權風險。

3

結語

目前我國童裝企業逾萬家,市場較為分散,面對童裝市場日益激烈的競爭,嘉曼服飾的市佔率還較低,資本實力與國內同行業上市公司相比,仍存在一定的差距。總的來看,公司的整體經營情況向好,但從毛利率和收入構成來看,公司對授權品牌依賴程度較高,而自有品牌的運營能力還有待提升,未來公司仍需加大線上運營的管理,做好成本控制,以提升自有品牌的盈利能力。

More Content