上半年,國內紡織服裝市場穩步復甦。年初至今,SW紡織服裝行業跑贏大盤0.32pct,1-7月,國內年服裝鞋帽、紡織品類社會零售總額達到7673億元。細分中高端女裝市場同步受益,國內中高端女裝頭部公司增勢顯著。

8月27日,國內中高端女裝龍頭贏家時尚發佈中期業績公吿,各項數據繼續領跑行業。公吿顯示,上半年公司實現收益30.78億元(人民幣,單位下同),同比增長53.66%,在已公佈業績的中高端女裝公司中收入規模第一,增速第二;毛利22.62億元,同比增長53.26%;實現純利2.8億元,同比大增134.21%,增速領跑行業。

營收、淨利雙雙大增的背後,公司多元產品矩陣和全渠道佈局戰略功不可沒。

一、多品牌齊頭並進,向平台化架構的品牌管理公司進化

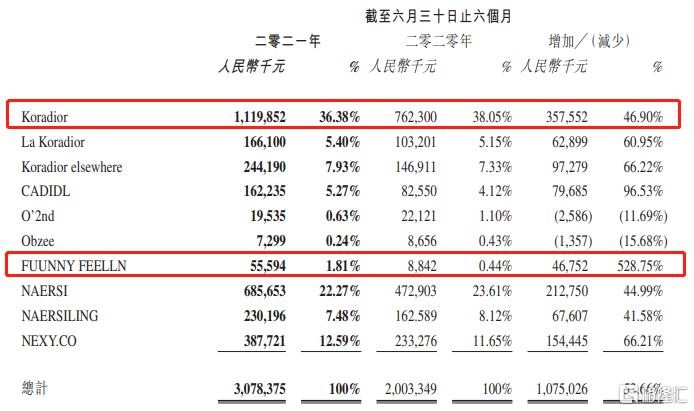

作為中高端女裝賽道的深耕者,贏家時尚深諳單一品牌的侷限性,較早地進行了多元的產品佈局,目前已經建立由Koradior、La Koradior、Koradior elsewhere、NAERSI、NAERSILING、NEXY.CO、CADIDL、FUUNNY FEELLN構成的產品矩陣。

上半年,贏家時尚的多品牌戰略再次奏效,八大品牌齊頭並進,對公司業績形成穩固支撐。

其中需要重點提到的是,Koradior及NAERSI品牌迅速復甦,銷售額分別達11.2億元、6.86億元,再次顯示出雙主力品牌強大的市場影響。主打高性價比的FUUNNY FEELLN品牌藉助渠道佈局和產品迭代,銷售額銷售額突破到5559.4萬元,同比暴增528.75%,已經為贏家時尚打開新的市場空間。

(來源:上市公司)

FUUNNY FEELLN能在短時間內形成可觀的業績貢獻,再次驗證了贏家時尚強大的品牌孵化能力,驅動公司向平台化架構的品牌管理公司轉變。而公司較低的負債比率和強勁的現金流入,也將對公司後續品牌矩陣的繼續擴張形成有力支撐。

這意味着公司成長天花板已經全面打開,後續可以通過自主創立或在市場尋覓合適標的等方式,迅速有效地切入更大的市場,持續驅動業績高速增長。

二、全渠道佈局,線上業務爆發可期

新零售和疫情影響下,人們的消費習慣已經出現不可逆的改變。在以“人”為核心的主流商業模式下,面對個性化的消費者,跨渠道的消費習慣,實時變化的互動需求…如何獲取更大的流量,再將流量最大化地轉化為銷量,成為消費領域共同思考的問題。對此,全渠道是接受度較高的解題思路。

反應在贏家時尚,其上半年在以直營門店建設為核心的基礎上,同步加快了經銷和線上平台投入力度。上半年公司直營門店新增70家,提升至1490家,對上半年業績貢獻高達80%,仍是業內直營門店數最多的公司。經銷商由去年年底的414家增加到445家,分銷渠道收益達2.27億元,同比增長366.41%。

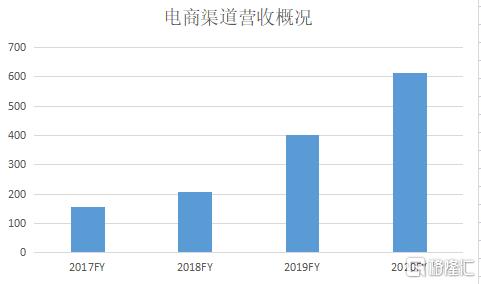

與此同時,電商渠道的收益達到3.86 億元,同比增長41.70%,已完成去年全年電商渠道營收的63.28%,為電商渠道全年營收的增長奠定了良好基礎。2017年-2020年間,公司電商渠道在總營收中的佔比已由7.1%提升至11.5%,重要程度不斷提升。

(來源:格隆匯)

在電商板塊,除了天貓商城、唯品會等傳統第三方電商平台,贏家時尚在2020年還推出了EEKA時尚商城小程序,補全了私域流量板塊,為電商渠道的全面增長奠定了基礎。尤其是疫情之下,公司轉變思維,將線上渠道的定位從原本的清貨為主,逐漸轉變為正價銷售新品的平台,有效提升了公司利潤標。其全新推出的EEKA時尚商城小程序更開放了庫存、會員、營銷資源等關鍵要素的共享機制,推出當年就實現營收3267萬元,展現出不俗的爆發力。

隨着線上線下業務的深度融合貫通,贏家時尚的全渠道佈局將繼續提升公司運營效率,成為拉動公司業績增長的重要引擎。

小結

根據招商銀行與貝恩公司聯合發佈的《2021中國私人財富報吿》,2018-2020年中國高淨值人羣(可投資資產超1000萬元)的年均複合增長率達到15%。預計2021年底,中國高淨值人羣數量將繼續增長至296萬人,國內高端消費品市場藴藏着相當大的增長潛力,中高端女裝將延續行業景氣度。

(來源:格隆匯)

但對於這樣一家既有現在又看得見未來的公司,資本市場的認知並不充分。贏家時尚當前市盈率(TTM)僅10.15倍,遠低於具有多品牌管理平台屬性的安踏、華住集團分別高達48.96倍、167.29倍的估值。即使是在中高端女裝行業內部,贏家時尚的市盈率和市銷率,也均低於可比中高端女裝賽道上市公司的平均估值水平。

隨着贏家時尚的業績持續兑現,其發展邏輯和商業前景將進一步得到驗證,市場終將認識到其估值與業績的明顯錯配,並予以改善。

More Content